Fintech Revolution

Fintechs and Neobanks: Beyond Transactions

Fintechs and neobanks have reshaped banking by offering fast, low-cost, and digital-first financial services. Platforms like Nubank, Revolut, and Paytm have attracted millions of customers by offering real-time payments, fee-free banking, and seamless user experiences. Payment networks such as UPI in India and PIX in Brasil have set new transaction speed and efficiency benchmarks. However, while fintechs and neobanks have excelled in transactional banking, they struggle to develop deeper, long-term customer relationships compared to traditional banks.

The 'Broaden and Deepen' Challenge

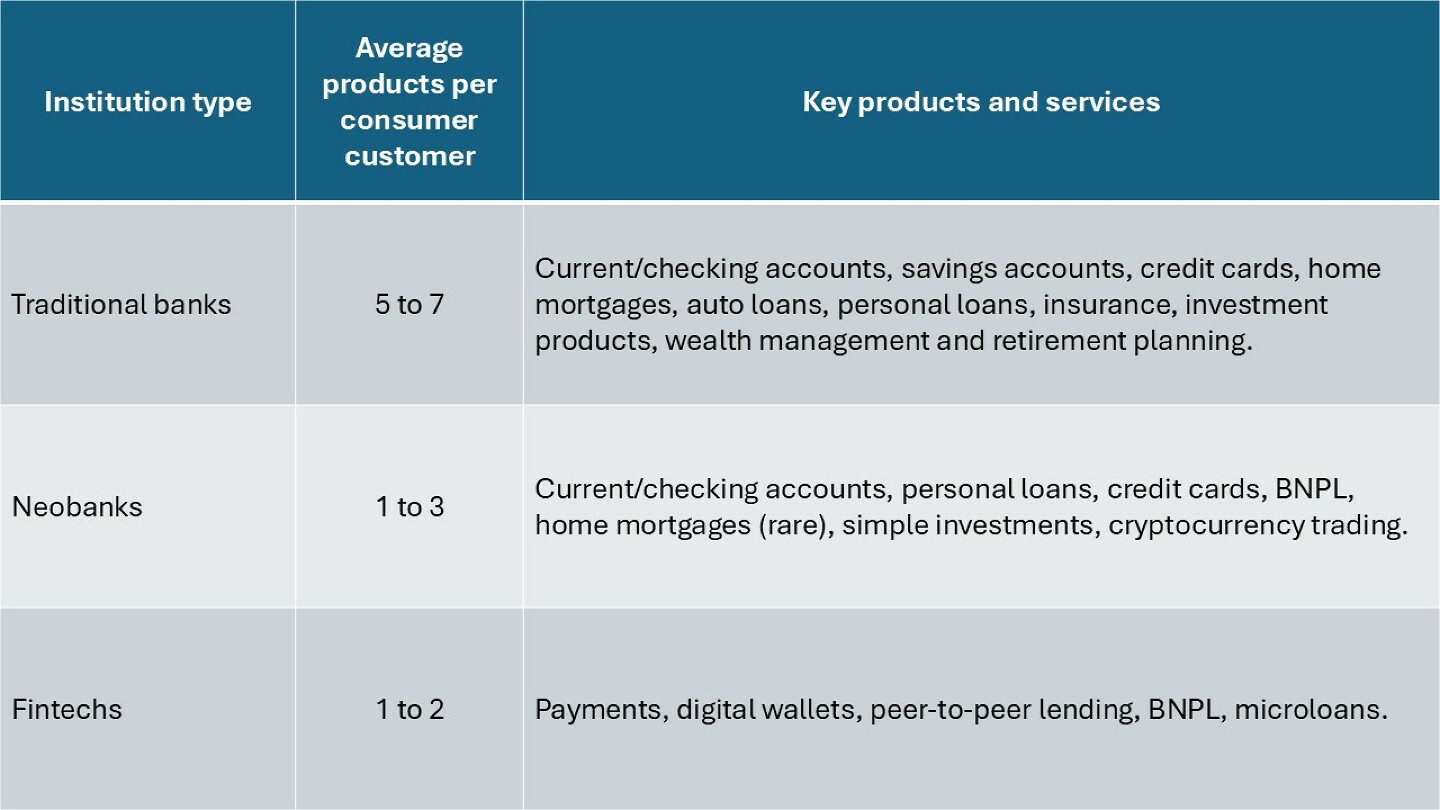

Traditional retail banks have mastered customer retention by offering a full spectrum of financial products. Most customers typically start with a current/checking account and progress to savings accounts, credit cards, mortgages, and investment products. Banks use CRM systems and data analytics to anticipate needs and deliver personalised recommendations, leading to an average of five to seven financial products per customer, far more than fintechs and neobanks.

This comparison highlights why traditional banks maintain higher customer retention, offering a full range of financial solutions ensures that customers do not need to switch providers as their financial needs evolve.

Fintechs, in contrast, primarily focus on payments, digital wallets, and unsecured lending, maintaining relationships across just one to three products. While this specialisation drives growth, it limits customer 'stickiness'. Without broader product offerings, fintechs risk losing customers to traditional banks when they seek long-term financial solutions like home financing or wealth management.

Trust, Relationship Building, and Customer Loyalty

Traditional banks have a strong trust advantage, particularly in regions where financial relationships are deeply valued, such as Japan, India, and the Middle East. Customers rely on human advisors, loyalty programs, and personalised service for complex decisions like home loans, retirement planning, and business financing.

Fintechs and neobanks, by contrast, rely on self-service models and chatbots, which, while efficient, lack personal engagement or have difficulty dealing with more complex situations. Younger generations may prefer digital-first banking, but older customers and high-net-worth individuals still value human interaction. Some fintechs and neobanks are addressing this by integrating AI-driven insights with human advisors to create hybrid banking experiences that blend efficiency with personalised support.

What the Future Holds: The 2030 Outlook

By 2030, fintechs and neobanks must move beyond transactions to build deeper customer relationships. Key areas of transformation will include:

- Expanding product ecosystems: Fintechs and neobanks must offer mortgages, investment products, insurance, and business banking. This will be achieved either through in-house development or strategic partnerships with traditional banks.

- AI-driven CRM and personalisation: Hyper-personalisation will define the next phase of fintech growth. AI-driven financial assistants will analyse spending habits, predict needs, and proactively suggest relevant products.

- Embedded finance and super apps: Fintechs will integrate financial services into social media, messaging apps, and e-commerce platforms, enabling seamless banking experiences within platforms like WhatsApp and Amazon.

- Blended digital-human banking models: The future will favour fintechs that combine AI-driven recommendations with human advisory services, particularly for wealth management and complex financial needs.

Collaboration, Not Competition

Rather than competing head-on, the future of banking will be defined by collaboration between fintechs, neobanks, and traditional banks. This has been recognised by some regulators in India and Singapore for instance, who have recommended applications for new banking licences from collaborations between fintechs, telcos and banks.

By 2030, successful financial ecosystems will be built on partnerships that leverage fintechs' agility and innovation alongside banks' extensive product portfolios and regulatory expertise. Fintechs and neobanks can integrate their seamless digital experiences, AI-driven insights, and embedded finance capabilities with full-service banks that provide mortgages, investment products, and financial planning. Meanwhile, traditional banks can adopt fintech innovations to enhance digital services and attract younger customers.

The future of banking will not be about winners and losers but about building integrated, customer-centric ecosystems. Institutions that embrace collaboration will be best positioned to deliver holistic financial experiences, ensuring customers stay engaged across their entire financial journey.