Advanced Operations and IT

Customer Data Management

In the evolving landscape of banking, a customer-centric digital retail bank is a modern institution that places customer needs, preferences, and experiences at the heart of its operations. By using cutting-edge technologies, data management practices, and digital platforms, such banks aim to create personalised, seamless, and omnichannel experiences that span both digital and physical service delivery. At the core of this transformation is customer data, which drives personalisation, customer engagement, and the overall digital strategy of the bank.

As we will discuss, banks are moving away from the restrictions of traditional structured, mainly demographic data towards highly-contextual unstructured data that provides better insight into customers' intentions, attitudes and behaviours. This offers banks richer context, relevance and personalisation opportunities than structured data, which is limited to fixed fields like age, income, or location.

Before all of this there are some foundations that must be in place. Building a customer-centric digital retail bank requires a well-thought-out data governance framework, effective data storage technologies, and robust systems for managing the flow of data across various departments, products, and services. These technologies must enable a holistic view of the customer, foster a culture of personalisation, and ensure compliance with stringent regulations. In this section, we will explore the key components of building such a bank, focusing on how customer data powers personalised experiences, the role of data governance in protecting and managing that data, and the storage technologies that enable data flow and actionable insights.

Customer-centricity: The Role of Customer Data

At the core of a customer-centric digital retail bank is a wealth of data about customers. This data is collected from a variety of touchpoints: for example, online banking interactions, mobile app usage, debit card, credit card and ATM transactions, chatbots and contact centre interactions, email communications, customer feedback surveys, and even social media comments. This data is leveraged to drive personalisation, omnichannel experiences, proactive engagement, and smarter decision-making across all aspects of the bank's operations.

Data is not only central to personalising digital interactions but also essential in maintaining the integrity and security of physical interactions. Customer-centric banks use data to improve physical service delivery, ensuring customer identities are verified across all touchpoints and financial products are aligned with individual customer needs.

The Importance of a Strong Data Governance Framework

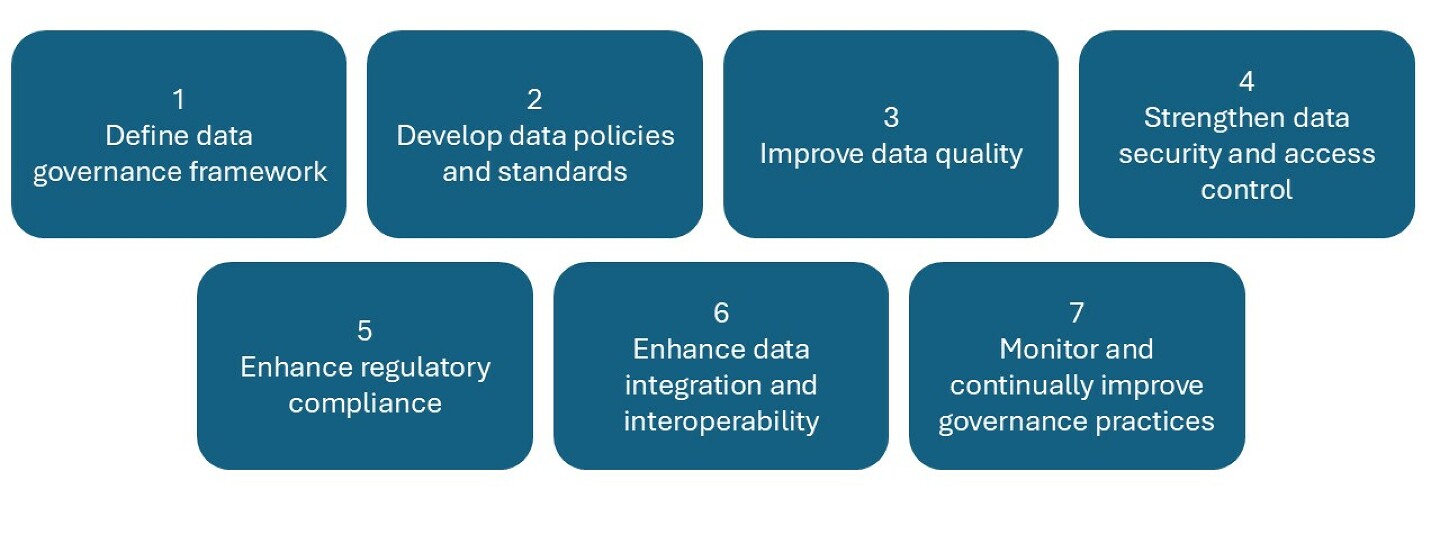

To realise the potential of customer data, it is crucial that retail banks have a robust data governance framework in place. Data governance ensures the quality, security, privacy, and compliance of customer data, providing a foundation upon which a customer-centric strategy can be built. A well-defined data governance framework is especially important given the regulatory pressures in the financial industry, such as regulations governing data privacy. The process looks like this:

Core Components of a Data Governance Framework

- 1. Data quality management: A customer-centric approach relies on the availability of clean, accurate, and complete data. Poor data quality can result in wrong customer segmentation, inaccurate recommendations, and trust issues with clients. Data governance frameworks ensure that the data banks collect is consistent and updated through rigorous data validation and cleansing processes.

- 2. Data security and privacy: Protecting sensitive customer information, such as banking credentials and personal details, is paramount. Data governance ensures robust security protocols, access controls, and encryption techniques are in place to prevent unauthorised access or data breaches. Data privacy protocols also ensure compliance with local and international regulations, establishing mechanisms like anonymisation and role-based access to protect customer data.

- 3. Compliance and risk management: Data governance practices are essential for adhering to regulatory standards in the financial sector. Compliance rules such as GDPR, PCI DSS, and AML regulations dictate how customer data must be handled, stored, and shared. A customer-centric bank must ensure that its data practices are transparent and compliant with these regulations by implementing audit trails, compliance reporting, and automated policy enforcement mechanisms.

- 4. Data lineage and transparency: Understanding where data comes from, how it moves, and who accesses it ensures transparency in customer data usage. Proper data lineage helps organisations track the flow of information across systems, which is crucial for operational efficiency, fraud detection, and regulatory reporting. Data transparency also fosters customer trust, as clients are more likely to engage with a bank that is open about how their data is used.

- 5. Data access and ownership: Clear protocols around data ownership and access rights are critical for managing customer data effectively. Not only must employees have access to relevant data, but they must also have the necessary permissions to use that data in a compliant and secure manner. Role-based access control (RBAC) ensures that data is accessed only by authorised personnel, reducing the risk of insider threats and unauthorised usage.

- 6. Data governance committee: Many banks establish a data governance committee, comprising compliance officers, IT security teams, and senior business leaders, to oversee data policies and ensure adherence to governance standards. This committee is responsible for updating policies as regulatory requirements evolve and ensuring that customer data is used ethically and effectively.

Effective governance of data will help the bank protect customer privacy, ensure compliance, and, importantly, foster trust, the cornerstone of customer-centric banking.

Data Storage Technologies: Key Components

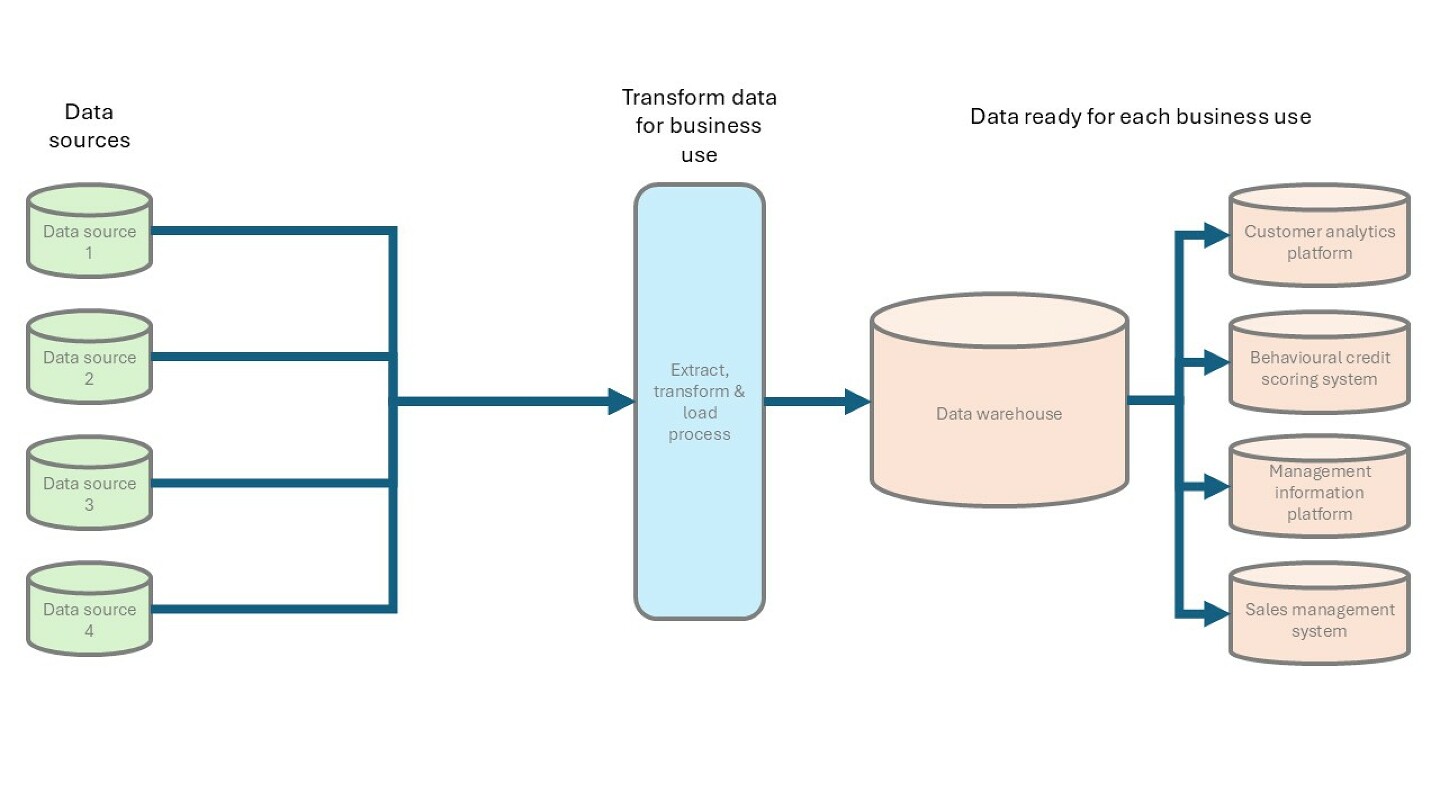

For a retail bank to be customer-centric, it needs a centralised data architecture that allows data to flow seamlessly across various platforms, departments, and applications. The bank's data infrastructure must be scalable, flexible, and capable of processing vast amounts of customer data from multiple sources. This is where data storage technologies come into play.

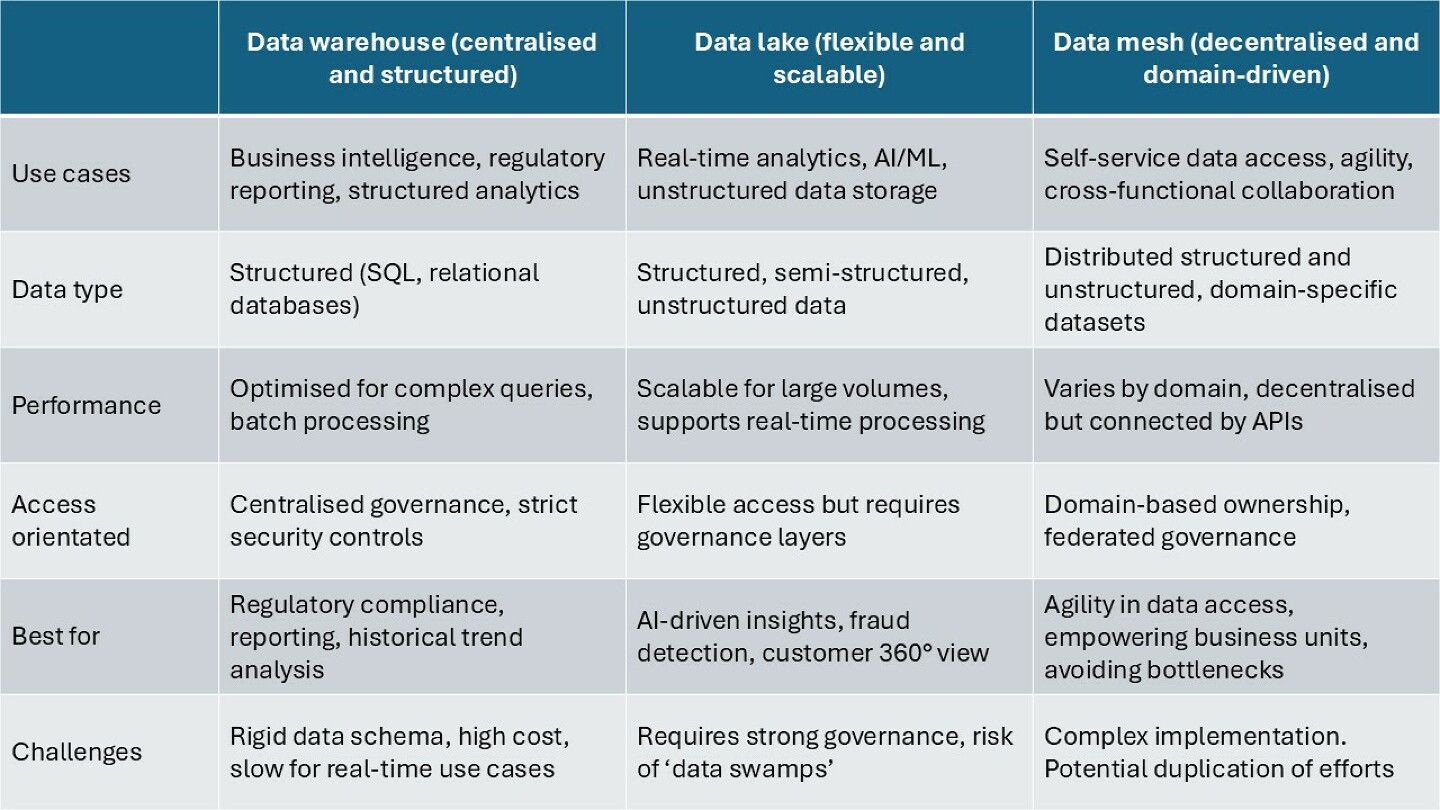

Data Warehouses: Storing Structured Data for Analytical Insights

A data warehouse is an essential component of any modern bank's data architecture, designed to store structured data from various systems (e.g., core banking, CRM, and transactional data). Data warehouses are used primarily for business intelligence (BI) and advanced analytics that provide insights into customer behaviour, spending patterns, and preferences.

Data warehouses allow banks to consolidate and organise data from disparate sources into a unified, relational database that supports online analytical processing (OLAP). By using SQL queries (a programming language that manages relational databases that organises structured data into tables with rows, columns, and defined relationships between them, by 'querying, inserting, updating, and deleting data), banks can generate detailed compliance and regulatory reports. However, because of their high degree of structure and accuracy they're not ideal for today's dynamic data-led environment where real-time assessment of structured and unstructured operational data and decisioning is crucial.

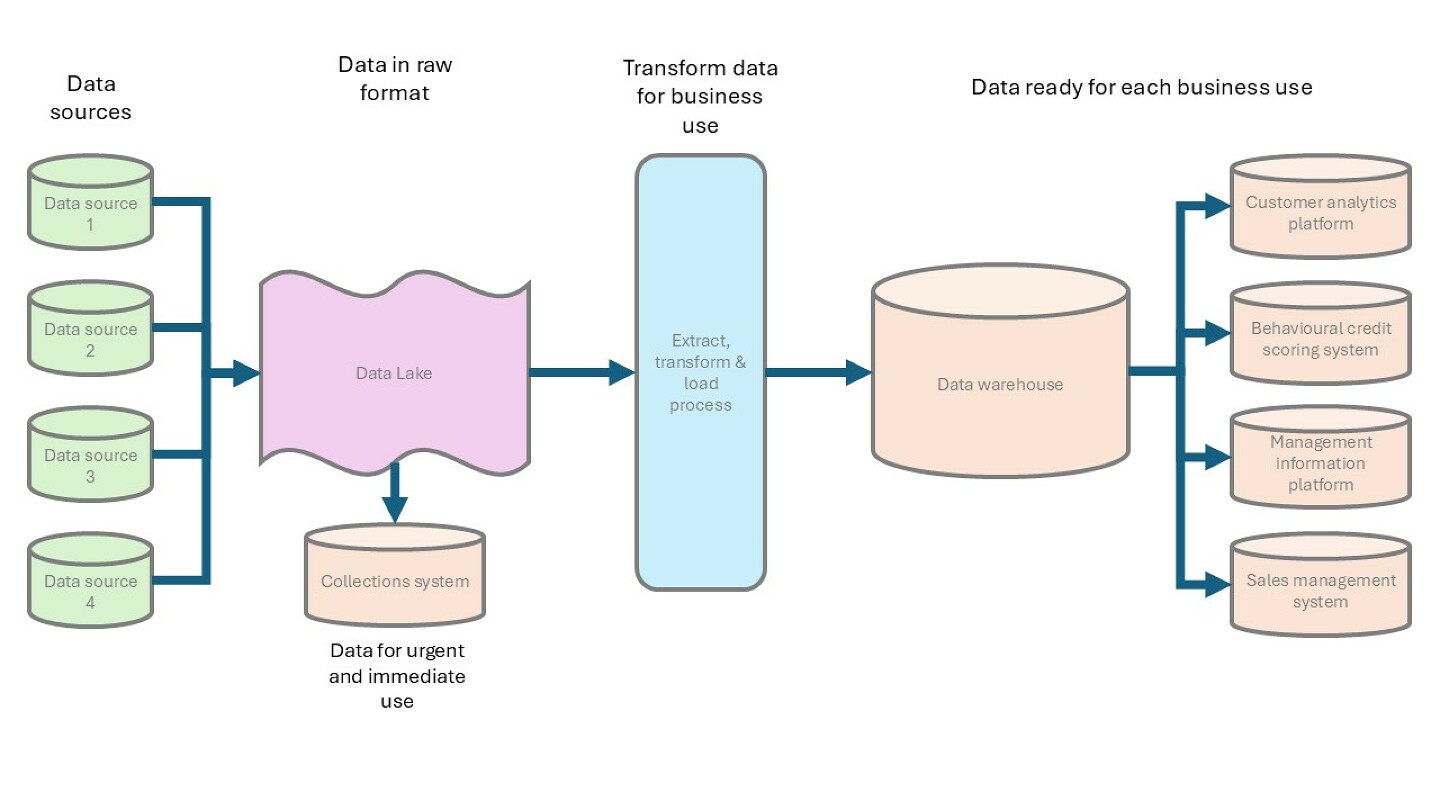

Data Lakes: Managing Unstructured and Semi-structured Data

While data warehouses are ideal for structured data, data lakes are designed to store structured, unstructured and semi-structured data such as customer emails, contact centre mobile app conversations, mobile app logs, social media comments, and multimedia content. Data lakes offer significant flexibility in how data is stored and processed, making them ideal for big data analytics and AI-driven decisioning and personalisation.

An example would be a collections and recoveries function where customers respond with repayment through SMS or WhatsApp messages or by calling and it is important to keep for legal reasons, their commitment to pay the late instalment or debt in a text format (without employees having to manually transcribe it) should follow-up collection or recovery be required.

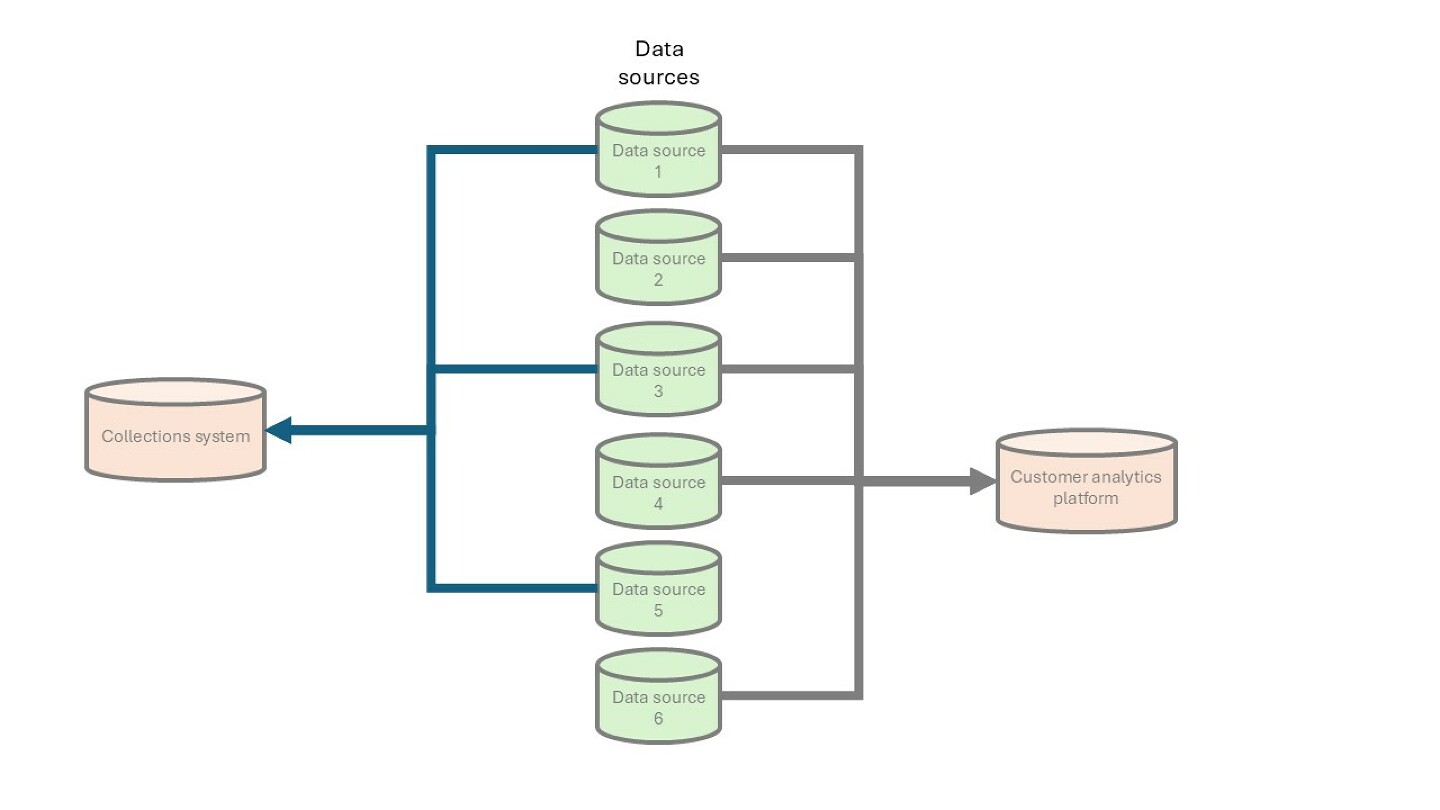

Data Mesh: Decentralised Data Ownership and Access

A data mesh decentralises data ownership and management, allowing each business unit (domain) to own and manage its own data while ensuring interoperability across the organisation. This approach improves agility, enabling faster insights and real-time decision making without reliance on a centralised data team. In this example, the collections team might process data in real-time to understand the effectiveness of today's collection activity to make adjustments to improve results.

How Banks Integrate Data Storage Technologies

It's a big step from relying on slow, batch processing of historic data through a data warehouse to real-time insight from data lakes or data mesh. However, no technology provides a total solution, and it is important that banks apply the right solution to the right problem. As banks increasingly implement real-time AI-powered processes they need real-time access to data. The following table outlines how banks create a modern data storage infrastructure.

Using Structured Data and Unstructured Data

In today's customer-centric digital banking environment, data is the foundation of every decision, interaction, and innovation. Retail banks rely on two main types of data, structured and unstructured, to personalise services, mitigate risks, and optimise customer experiences. While structured data has traditionally been the primary source of insights, unstructured data is emerging as a critical competitive advantage, enabling banks to deliver real-time, highly personalised, and proactive services.

To understand the importance of leveraging both structured and unstructured data, it is essential to explore their differences, the technologies that make unstructured data usable, and how banks can turn vast amounts of raw customer information into actionable insights.

Structured Data vs Unstructured Data

In banking, customer data can be broadly classified into structured and unstructured categories, each with its own characteristics, advantages, and challenges.

Structured Data

This refers to information that is organised, formatted, and stored in relational databases. It includes data such as transaction records, customer demographics, account balances, and CRM system inputs. This type of data accounts for approximately 30% to 40% of total customer data in the banking sector.

Structured data is easy to analyse, supports regulatory compliance and operational management, and enables basic customer segmentation. However, it is often limited to predefined categories and lacks real-time contextual understanding.

Key technologies used to manage structured data include SQL databases, CRM platforms, and traditional business intelligence tools. It supports structured interactions such as marketing campaigns and loan approvals and plays a foundational role in identifying unusual transaction patterns for fraud prevention.

While structured data contributes to efficient operations and regulatory reporting, its potential for personalisation is moderate, mostly based on historical information and demographics, and falls short in delivering truly personalised experiences.

Unstructured Data

On the other hand, unstructured data makes up 60% to 70% of customer data in banking and includes raw, diverse information that lacks a predefined format. Examples include call centre transcripts, chatbot conversations, social media posts, and mobile app usage logs. It can provide deeper insights into customer intent, behaviour, and sentiment.

While it is more complex to store and analyse, requiring advanced technologies like NLP and ML, real-time data streaming and sentiment analysis, it offers significant competitive advantages.

Unstructured data enables real-time personalisation, proactive fraud detection through voice and text analysis, and monitoring of social media for fraudulent activities. It supports hyper-personalisation, allowing banks to engage customers in real time and deliver tailored services.

Although challenging to manage, unstructured data is critical to the future of banking, driving enhanced customer engagement, predictive services, and next-best-offer strategies.

In summary, while structured data remains essential for operational and regulatory compliance needs, unstructured data is increasingly vital for delivering a hyper-personalised, responsive, and predictive banking experience that will set the bank apart from competitors.

Why Harnessing Unstructured Data is a Competitive Advantage

Unlocking Hidden Customer Insights

Unstructured data provides rich qualitative information that structured data alone cannot capture. For example, a structured dataset may indicate that a customer frequently checks loan rates but does not apply. An unstructured dataset, such as chatbot logs or call transcripts, may reveal that the customer is concerned about approval criteria or prefers lower monthly repayments.

By analysing customer conversations, feedback, and engagement patterns, banks can refine product offerings and personalise financial advice to meet customer needs more precisely.

Enhancing Fraud Detection and Risk Management

Fraud detection traditionally relies on structured data, such as monitoring unusual transactions, but criminal tactics evolve rapidly. By integrating unstructured data sources, banks can use AI-powered voice and text analysis to detect stress, hesitation, or deception in fraud investigations, analyse social media activity for signs of compromised accounts, and monitor dark web discussions for leaked banking credentials.

For instance, if a customer calls a bank to report a stolen card, voice biometrics can analyse the stress in their tone to verify if they are truly the account holder or a fraudster attempting social engineering.

Delivering Real-time Hyper-personalisation

A customer-centric digital bank must adapt services dynamically to individual preferences. Structured data helps identify demographics and transaction history, but unstructured data provides real-time context, such as how a customer navigates a mobile app, what questions they ask a chatbot, and what sentiment they express on social media about their banking experience.

By processing this data with NLP, banks can offer context-aware, personalised financial recommendations, increasing engagement and retention.

Strengthening Customer Trust and Relationship Management

Customers expect their banks to be proactive and responsive. If a bank can detect dissatisfaction from call centre logs or chatbot interactions, it can intervene before a customer decides to leave. AI-powered voice analytics can detect frustration or stress in a customer's tone and escalate calls to senior advisors, while sentiment analysis of emails and social media can flag unhappy customers for personalised outreach.

Predictive analytics can suggest account recovery offers if a customer shows signs of disengagement. This data-driven relationship management fosters loyalty and enhances customer lifetime value.

Competitive Differentiation in an AI-driven Hyper-personalised Era

Many traditional retail banks struggle to use unstructured data, creating an opportunity for agile, digital-first banks to differentiate themselves. Fintech disruptors already use AI to automate real-time credit scoring based on alternative data, provide AI-driven financial coaching using chatbot interactions, and offer context-aware banking alerts based on unstructured transaction notes.

Banks that embrace unstructured data can outperform legacy competitors by delivering faster, more personalised, and predictive financial services.

Technology That Makes Unstructured Data Usable

To fully leverage unstructured data, banks must adopt modern data architectures that provide scalability, real-time processing and analytics and AI-driven processing tools. Data architecture examples include 'data lakehouses' (blending data lakes and warehouses), real-time data streaming, microservices (separate data stores per service), and data mesh. Each optimises data management for agility, governance, and efficiency.

NLP enables chatbots, virtual assistants, and automated customer support by analysing text and speech. ML algorithms detect patterns in unstructured customer interactions for fraud prevention and personalisation.

Real-time data streaming tools process live transaction logs, chatbot messages, and customer calls instantly. Data lakes store vast amounts of raw, unstructured customer data, such as emails, voice logs, and social media, for later analysis. AI-powered sentiment analysis monitors social media, call centre interactions, and surveys to gauge customer emotions.

By integrating these technologies, banks turn unstructured data into actionable insights, enhancing customer experience and operational efficiency.

Data-driven Banking as a Competitive Edge

A customer-centric digital retail bank must use both structured and unstructured data to remain competitive. Structured data enables efficient operations and regulatory compliance, while unstructured data unlocks real-time insights, deeper personalisation, and predictive capabilities.

Banks that master unstructured data gain the ability to understand customer sentiment and intent, predict financial needs and risks, and deliver highly personalised, AI-powered banking experiences. They also stay ahead of evolving fraud tactics and build stronger customer relationships.

As the financial industry shifts towards AI-driven digital banking, the ability to process and act upon unstructured data will define market leaders. Banks that embrace next-generation data architectures will not only drive better customer engagement but also build more resilient, intelligent, and responsive banking ecosystems.