Advanced Customer Management - Building Customer Management Capabilities

NPS and Other Customer Feedback Metrics

Net Promoter Score (NPS) is a widely adopted tool in retail banking for measuring customer loyalty and satisfaction. It gauges the likelihood of customers recommending a bank's products or services to others. However, while NPS provides valuable insights into customer loyalty, it does not tell the full story. To truly understand the customer experience and make actionable improvements, banks should use NPS in conjunction with other customer feedback metrics.

1. Net Promoter Score (NPS)

Like Michael in the scenario, have you ever received an email or message with this question?

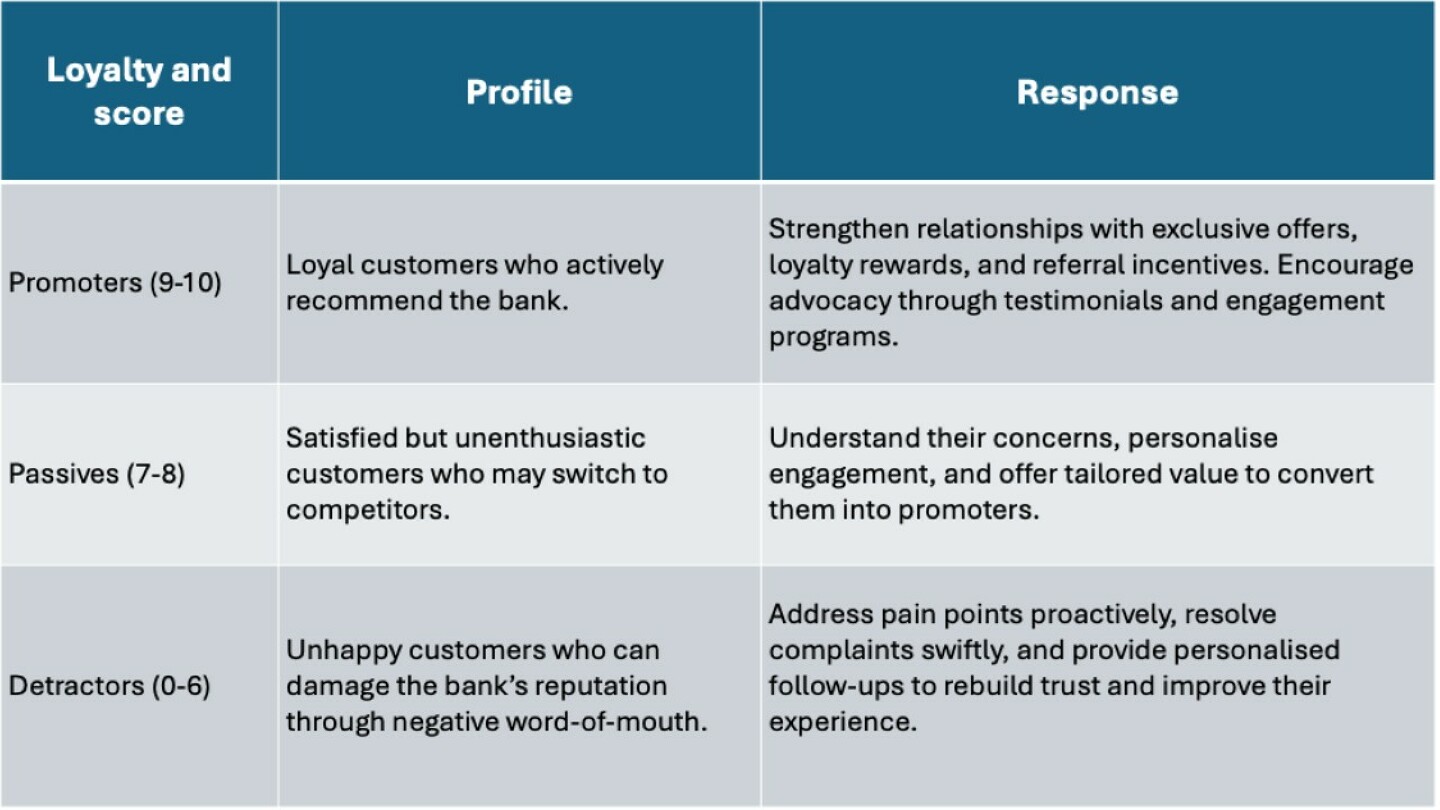

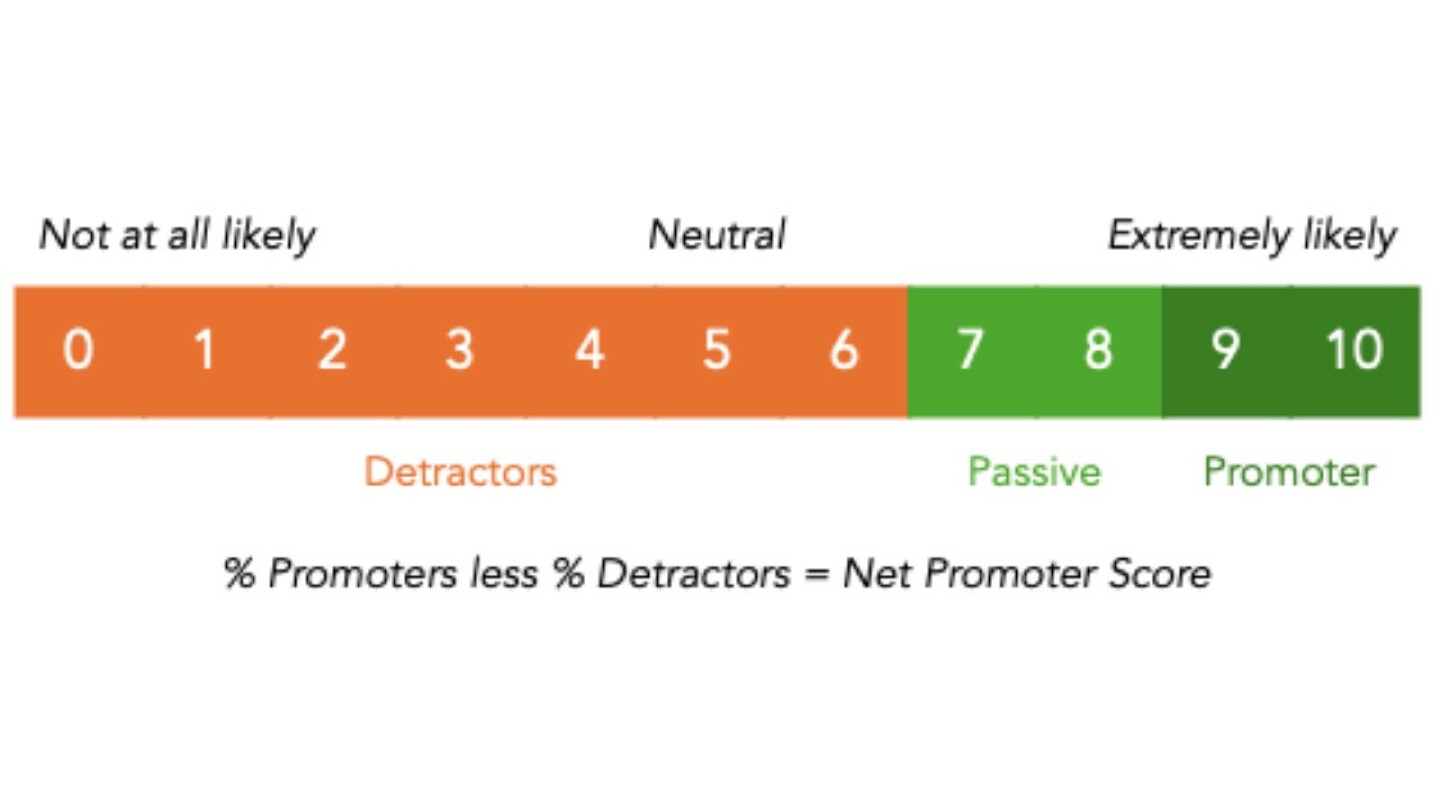

From their responses to this question, NPS categorises customers into three groups:

Below we have an NPS outline:

NPS is valuable because it is a simple question that provides a quick snapshot of customer loyalty and helps to identify areas for improvement. Retail banks can use NPS to assess the success of their services, track customer sentiment over time, and recognise the need for change in their operations.

NPS also outlines engagement approaches (see above) for each group to grow the number of promoters and reduce the number of detractors. Detailed analysis of the unstructured data in the text box using AI-powered tools that we discuss in 'Operations and IT – Change the Bank' module allows banks to address individual customer concerns and identify trends that help them improve their service.

Because it takes time for customers to become loyal, NPS should be used on a quarterly or biannual basis to track changes and the impact of service or product improvements.

However, the challenge with NPS is that it doesn't provide insight into the reasons behind customer satisfaction or dissatisfaction. This is where complementary feedback metrics come in.

2. Customer Satisfaction (CSAT)

CSAT measures how satisfied customers are with a specific interaction or product. It is often assessed through a simple question such as: "How satisfied were you with your experience today?" Customers rate their satisfaction on a scale from 1 to 5 or 1 or 7. It's similar in approach to NPS, but with a focus on satisfaction and improving processes or products.

There are no hard and fast rules for CSAT survey frequency, but customers must not be bombarded after every interaction. Banks should focus on key 'moments of truth' interactions to avoid survey fatigue (and a corresponding drop-off in quality and insight).

Why Use CSAT with NPS?

While NPS is a long-term loyalty measure, CSAT provides insight into specific touchpoints, such as a phone call with a customer service representative or an interaction on the mobile app. Combining NPS with CSAT helps banks identify the root causes of satisfaction or dissatisfaction, enabling them to fine-tune their services in specific areas like loan applications or customer support interactions.

Example: After a customer contacts the bank's call centre, the bank can use CSAT to assess the quality of the interaction and follow up with customers who had poor experiences, ensuring that they are satisfied and reducing the risk of negative NPS scores.

3. Customer Effort Score (CES)

CES measures how much effort a customer has to put forth to complete a task or resolve an issue. The typical question is: "How easy was it to resolve your issue today?" The scale ranges from "Very Difficult" to "Very Easy."

CES is useful for identifying operational pain points within the bank. A customer might be loyal (as shown by NPS) but might rate their experience poorly if the process was difficult or time-consuming. By combining NPS and CES, banks can pinpoint issues such as inefficient loan processing or complicated website navigation that may hinder customer satisfaction, even if overall loyalty remains strong.

CES should be used following operational interactions, such as completing an online quotation and/or applying for a new loan or logging on to online banking for the first time.

4. Customer Lifetime Value (CLV)

CLV predicts the total revenue a bank will generate from a customer throughout their relationship. It considers transaction frequency, average spend, account types, and relationship duration.

CLV helps banks understand the financial value of their customers. While NPS identifies promoters, passives, and detractors, CLV shows how valuable each customer is. By combining NPS with CLV, banks can focus their efforts on high-value promoters who are likely to provide the most long-term revenue. This ensures that the bank's retention strategies are tailored not only to improve loyalty but also to optimise profitability.

5. First Contact Resolution (FCR)

FCR measures the percentage of customer issues resolved during the first interaction. It's an important metric in customer service, as resolving issues quickly is one way to improve customer satisfaction.

FCR can directly influence a customer's NPS score. A customer who resolves an issue on the first contact is more likely to be satisfied and loyal. If a bank has a high NPS but poor FCR, it might indicate that while customers are loyal, they're frustrated by the number of touchpoints needed to resolve issues. Therefore, combining NPS with FCR allows banks to optimise their customer service processes and improve overall satisfaction.

6. Digital Satisfaction (App, Website, and Mobile)

Digital Satisfaction measures customer satisfaction with digital tools, including mobile apps, online banking, and websites. Customers rate their satisfaction with these specific tools to help the bank understand their digital experience.

As digital banking continues to grow, customer satisfaction with digital tools is a critical component of overall loyalty. By collecting feedback on digital channels, banks can identify areas where the user experience can be improved, leading to higher customer satisfaction and potentially better NPS scores – and much prized advocacy.

Example: If a customer enjoys using the bank's mobile app but finds the loan application process complicated, a low digital satisfaction score may indicate that the app experience could be simplified. This feedback, when combined with NPS, can highlight the need for specific improvements.

Using NPS with Customer Value Scores and Credit Risk Scores

Banks can significantly strengthen the value of NPS by integrating it with customer value scores and credit risk scores on their data analytics platform. These metrics offer insights into the financial importance of a customer and the potential risk they pose to the bank.

1. Customer Value Scores (CVS)

These scores help banks identify high-value customers based on factors such as revenue contribution, account types, transaction frequency, and engagement. Combining NPS with CVS allows banks to prioritise their highest-value promoters, ensuring they maintain strong relationships with the most profitable customers.

Example: A high-value customer who scores 10 on NPS should be offered personalised, high-end services or loyalty rewards to maintain their satisfaction and prevent churn.

2. Credit Risk Scores

Risk scores are used to evaluate the likelihood that a customer may default on loans, miss payments, or otherwise negatively impact the bank's profitability. If a customer is a detractor (score 0 to 6 on NPS) and also has a high credit risk score (i.e. they are a low default risk), the bank should take immediate action to address their dissatisfaction while mitigating financial risk. This could involve personalised outreach, tailored solutions, or targeted interventions to prevent churn and reduce risk exposure.

Example: If a customer has expressed dissatisfaction (NPS 4) but is also identified as a high credit risk scoring customer, the bank may proactively offer financial counselling or tailored loan restructuring options to retain the relationship and reduce risk.

Using NPS to Address Customer Segments

Once banks collect these various metrics, they can use NPS to address customer segments more effectively. Promoters should be engaged with loyalty programmes, personalised offers, and invitations to refer others. Passives can be targeted with incentives or feedback requests to nudge them toward greater loyalty, while detractors need to be carefully managed, ideally through personalised follow-ups or special offers to improve their perception of the bank.

By measuring CSAT, CES, and FCR, banks can identify specific areas that need improvement and adjust their strategies for improving customer satisfaction in targeted ways. Using CLV and Digital Satisfaction allows for more personalised, value-driven approaches to customer retention, ensuring that high-value customers are given priority, especially in a highly competitive market.

Conclusion: The Role of Customer Feedback Metrics

Retail banks must collect and analyse multiple customer feedback metrics to build a comprehensive view of the customer experience. NPS provides a broad view of loyalty, but metrics like CSAT, CES, FCR, and Digital Satisfaction offer deeper insights into specific areas of customer interactions. By combining these metrics, banks can continuously optimise their operations, reduce friction points, and offer personalised experiences that build customer loyalty and trust.

Integrating NPS with customer value scores and risk scores allows banks to prioritise high-value customers and mitigate potential risks, improving both profitability and customer satisfaction. These additional metrics not only help banks identify problems but also create actionable strategies that can improve retention and drive sustainable growth. As digital channels continue to dominate the banking landscape, integrating NPS with other metrics will become increasingly critical to meeting customer expectations and staying competitive.