Fintech Revolution

Redefining the Future of Retail Banking

Before we take part in the revolution, we should explain the roles of the key players.

Retail Banking Ecosystem

Traditional Retail Banks

Traditional banks rely on physical branches, legacy systems, and have heavier regulatory oversight. While fintechs, neobanks, and big tech emphasise innovation and customer-centricity, traditional banks are mostly product-centric (focusing on selling specific products, not customer needs) and must balance regulation, risk management, and an older technology infrastructure.

Fintechs

Fintechs are tech-driven companies offering specialised financial services like payments, lending, and investing: the majority of early fintechs offered either payments or lending services. They use cutting-edge technologies such as AI, blockchain, and cloud computing to provide faster, cheaper, and more user-friendly mobile-based services. Unlike traditional banks, fintechs usually focus on specific services, such as peer-to-peer payments or robo-advisory wealth management and are not bound by physical branches or legacy systems. But as we'll see, they need to expand their offerings to advance.

One of the drivers for payment fintechs is the first EU Payment Services Directive (PSD), adopted in 2007 and effective in 2009 (in 27 countries), standardised payment regulations across the EU, fostering competition, innovation, and consumer protection. It allowed non-bank providers to operate, enabling faster cross-border payments and setting the stage for open banking with PSD2 in 2015. Before PSD, firms like Western Union (telegraphing money since 1871, PayPal (originating in 1998), and Skrill (as Moneybookers from 2001) operated under national laws. Fintechs such as PayPal and Wise (2011, as Transferwise) disrupted banking by offering faster, cheaper payment services. PSD formalised non-bank Payment Institutions (PIs), creating a unified regulatory framework that enabled fintechs to scale across the EU, shaping modern digital payments.

Neobanks

Neobanks operate as digital-first banks, offering full banking services (current or checking accounts, payments, savings, personal or business loans, and home loans) to consumers and MSMEs with no physical customer-facing locations. They focus on lower fees, intuitive mobile experiences, and innovation. Neobanks typically provide simpler, more accessible services compared to traditional banks, and tend to have younger customers.

The first neobanks emerged globally in the late-2000s, driven by fintech innovation and regulatory shifts. Early examples include Simple (2009, USA), Fidor Bank (2009, Germany), Moven (2011, USA), N26 (2013, Germany) Nubank (2013, Brazil), and WeBank (2014, China). In Africa, early movers were TymeBank (2018, South Africa) and Kuda Bank (2019, Nigeria). The Asia-Pacific and Middle East regions saw Judo Bank (2016, Australia), GXS (Singapore, 2020) and YAP (2021, UAE) start to reshape banking.

Traditional Retail Bank, Fintech and Neobank Comparison

It is important to understand the differences and similarities of the three main players in the ecosystem. Traditional retail banks, fintechs and neobanks compete in the same markets for the same consumers and MSMEs. Each has distinct characteristics covering their revenue model and cost base; key advantages and disadvantages; challenges; and opportunities for revenue growth and cost reduction by 2030. These categories are not entirely exclusive. Fintechs can get full banking licences and evolve into neobanks, while some traditional banks launch standalone digital banks (eg, Chase UK).

(Big tech and telco mobile money operate on very different models and are excluded from the comparison but are summarised later in this section.)

Revenue Model

Traditional retail banks primarily earn revenue through net interest margins, account maintenance fees, and fees from wealth management and advisory services. Fintechs, on the other hand, rely on transaction fees, software-as-a-service (SaaS) or subscription models, interest income from lending (if applicable), and monetising customer data. Neobanks generate income through net interest margins, subscription fees for premium services, and interchange fees from card usage.

Cost Base

Traditional banks carry high costs associated with maintaining physical branches, employing customer-facing staff, complying with regulations, and operating legacy IT systems. Fintechs have a different cost structure focused on technology infrastructure, significant marketing expenses to acquire customers, and regulatory compliance, while aiming for operational efficiency. Neobanks share similar cost elements to fintechs but generally benefit from lower fixed costs due to their lack of branch networks and leaner operational models.

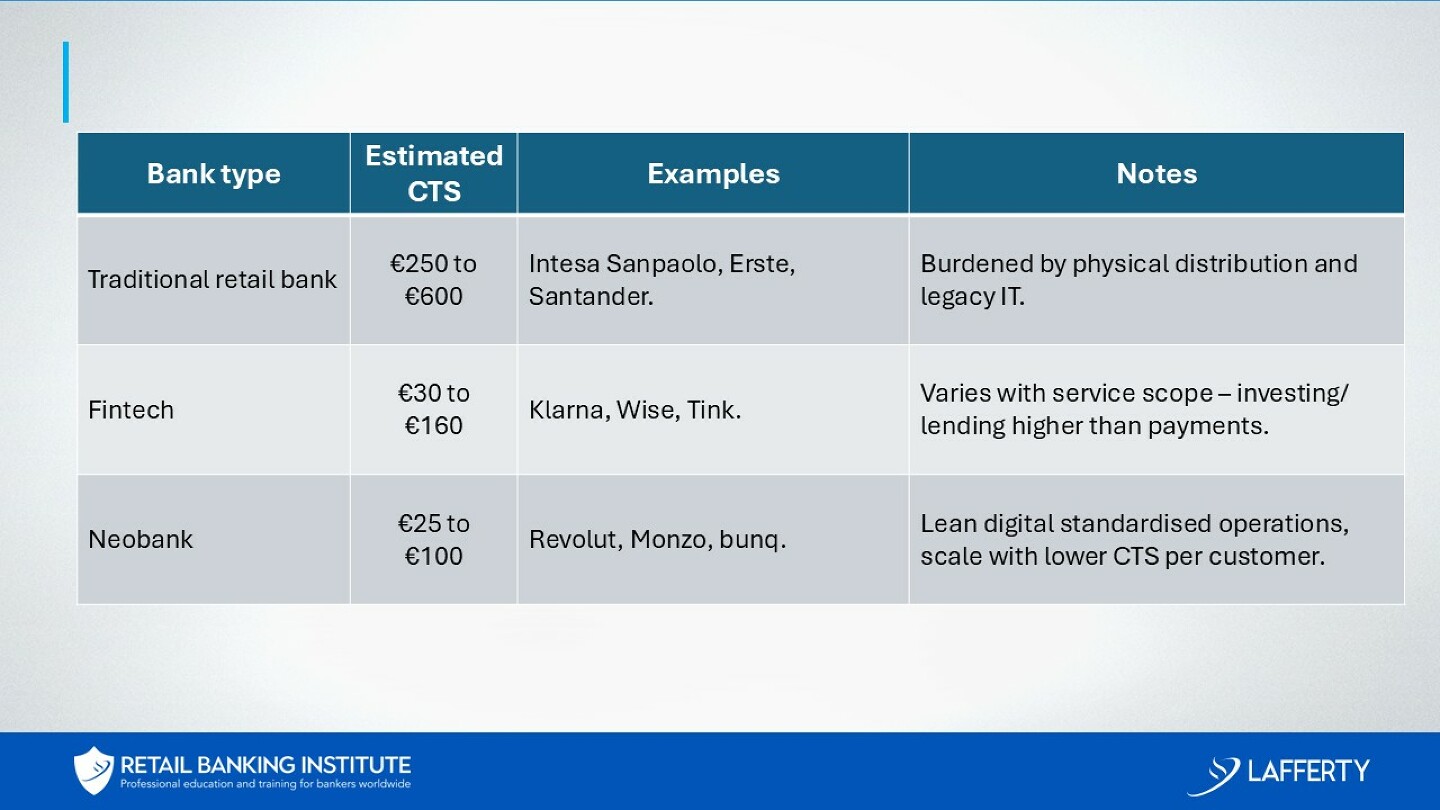

Traditional banks are burdened by physical branch networks that deliver face-to-face service, call centres and manual paper-based processes, siloed business functions and legacy IT systems that consume a greater proportion of costs to maintain them. Neobanks often achieve 60% to 85% lower 'cost to serve' (CTS) customers than traditional banks because of their economies of scale, fully digital onboarding, lean, automated and standardised operations and unified cloud-native platforms. Fintechs can exhibit a broad range of CTS ratios because of their different service scope, for example, investing and lending money will be higher than payments.

European CTS Averages

For comparison, the following table compares well-known European example of each type and their CTS and a brief explanation of the drivers.

Key Advantages

Traditional retail banks benefit from strong brand recognition, long-standing customer trust, a comprehensive suite of services, and well-developed compliance frameworks. Fintechs excel in agility and innovation, offering tech-driven, efficient solutions that can be scaled quickly and cost-effectively. Neobanks take advantage of their digital-first approach, benefiting from lower operational costs, ease of user experiences via mobile platforms, and the absence of expensive physical branches.

Key Disadvantages

As previously mentioned, traditional banks struggle with high infrastructure costs and slow adaptation to technological change, often held back by outdated legacy systems – though notably many banks are upgrading. Fintechs, despite their innovation, face intense competition, a strong dependency on technology, and high costs for customer acquisition, while remaining vulnerable to technical disruptions. Neobanks face challenges in building customer trust and brand awareness, offering fewer services compared to full-service banks.

Challenges to Overcome

Traditional banks must push forward with digital innovation so they can take advantage of data analytics and AI, and reduce their reliance on physical branches. Fintechs need to navigate regulatory compliance and address concerns around data privacy. Neobanks face the challenge of competing with traditional banks' established customer base and overcoming regulatory barriers to gain full banking licences.

Revenue Growth by 2030

Traditional banks are expected to see revenue growth by offering more personalised, digital services. Fintechs anticipate continued growth through the expansion of data-driven products and services. Neobanks are well-positioned to grow as consumer adoption of digital banking continues to rise.

Cost Reduction by 2030

Traditional banks will need to cut costs by reducing their branch networks and investing in technology optimisation. Fintechs are expected to further decrease expenses by scaling back physical infrastructure and enhancing operational efficiency. Neobanks are set to benefit from ongoing technological advancements that enable even greater cost efficiency.

Challengers: Big Tech and Telcos

Globally and regionally there are challengers to the traditional bank, fintech and neobank models: big tech and telcos, who want to monetise their customer bases without the regulatory burden.

Big Tech

Big techs, including Apple, Google, Amazon, and Tencent, integrate financial services like payments, credit, and insurance into their platforms, using their vast customer data and AI to create personalised financial products. Unlike traditional banks, big tech firms are platform-centric (ecommerce or social media) and focus on embedding financial services into their broader ecosystems, often prioritising convenience over regulatory complexity. Often banks rely on big tech at the back end: many banks now run on cloud services provided by big tech.

Big Tech makes money from financial services like payments and wallets primarily through merchant fees, partnerships with banks and card networks, and by boosting user engagement within their ecosystems. Services like Apple Pay, Google Pay, and Amazon Pay help retain users and gather valuable behavioural data to enhance advertising and product recommendations. They also monetise through co-branded cards, lending products, and tools for merchants. In emerging markets, companies offer low-cost or free services to build trust and embed themselves in daily financial activity, aiming for long-term gains in e-commerce, advertising, and digital infrastructure dominance.

Big Tech started to integrate financial services in the 2010s, reshaping fintech. Apple launched Apple Pay (2014) and Apple Card (2019), while Google introduced Google Pay (2018). Amason entered payments in 2007 and lending in 2011. Tencent pioneered WeChat Pay (2013) and WeBank (2014), expanding into digital payments, lending, and insurance, while Alipay also grew into a vast payments network.

Telcos Mobile Money

Both fintechs and mobile money telecoms offer digital financial services like payments and lending, promote financial inclusion, use technology and agent networks, and face growing regulatory attention in Africa.

Mobile money operators, such as M-Pesa, MTN MoMo, and Airtel Money act like fintechs, offering digital financial services like payments and lending, promote financial inclusion through technology, but with three key differences. They operate under telecom regulations, not banking ones, and unlike fintech startups, mobile money is a secondary business for them, finally, they rely on telecoms infrastructure rather than financial technology.

Their market dominance and regulatory influence resemble big tech firms, yet their core business remains telecoms and will continue in the future, just as big tech financial services is a secondary line of business. As they evolve into financial infrastructure players, regulators increasingly view them as systemic institutions, raising debates on whether they should be regulated like banks to ensure financial stability.

How did telcos mobile money evolve to become vital financial platforms? It evolved in developing countries to fill gaps left by traditional banks. High mobile phone use, low banking access, and demand for simple, safe financial services drove telecom-led innovation. Services began with money transfers and expanded to payments, savings, and credit, leveraging agent networks and mobile infrastructure.

The first telecom-based mobile money services included Smart Money (2000, Philippines), enabling SMS-based transactions, and M-Pesa (2007, Kenya), allowing money transfers and bill payments via mobile. Reliance Communications (2007, India) also launched a mobile wallet, paving the way for mobile financial services worldwide. M-Pesa still controls 90 percent of mobile money services in Kenya, while other countries such as Tanzania have mandated interoperability.

Telcos make money from financial services like payments and wallets through transaction fees on transfers, bill payments, and merchant payments. They earn interest on wallet balances held in partner banks and share in revenues from microloans, savings, and insurance offered through mobile money platforms. Telcos also monetise via partnerships with businesses and fintechs by providing APIs and bulk payment solutions.

Merchant services, agent networks, and customer transaction data enable additional revenue through cross-selling, scoring for credit, and targeted promotions. These financial services boost customer loyalty, increase mobile usage, and position telcos as key players in digital financial ecosystems, especially in emerging markets.

Some digital banks and new branch-based banks ranging from Capitec to Revolut and N26 have recently launched mobile data offerings to compete with telcos.