Advanced Customer Management - Building Customer Management Capabilities

Life Stage Analysis

Understanding Consumer Life Stages

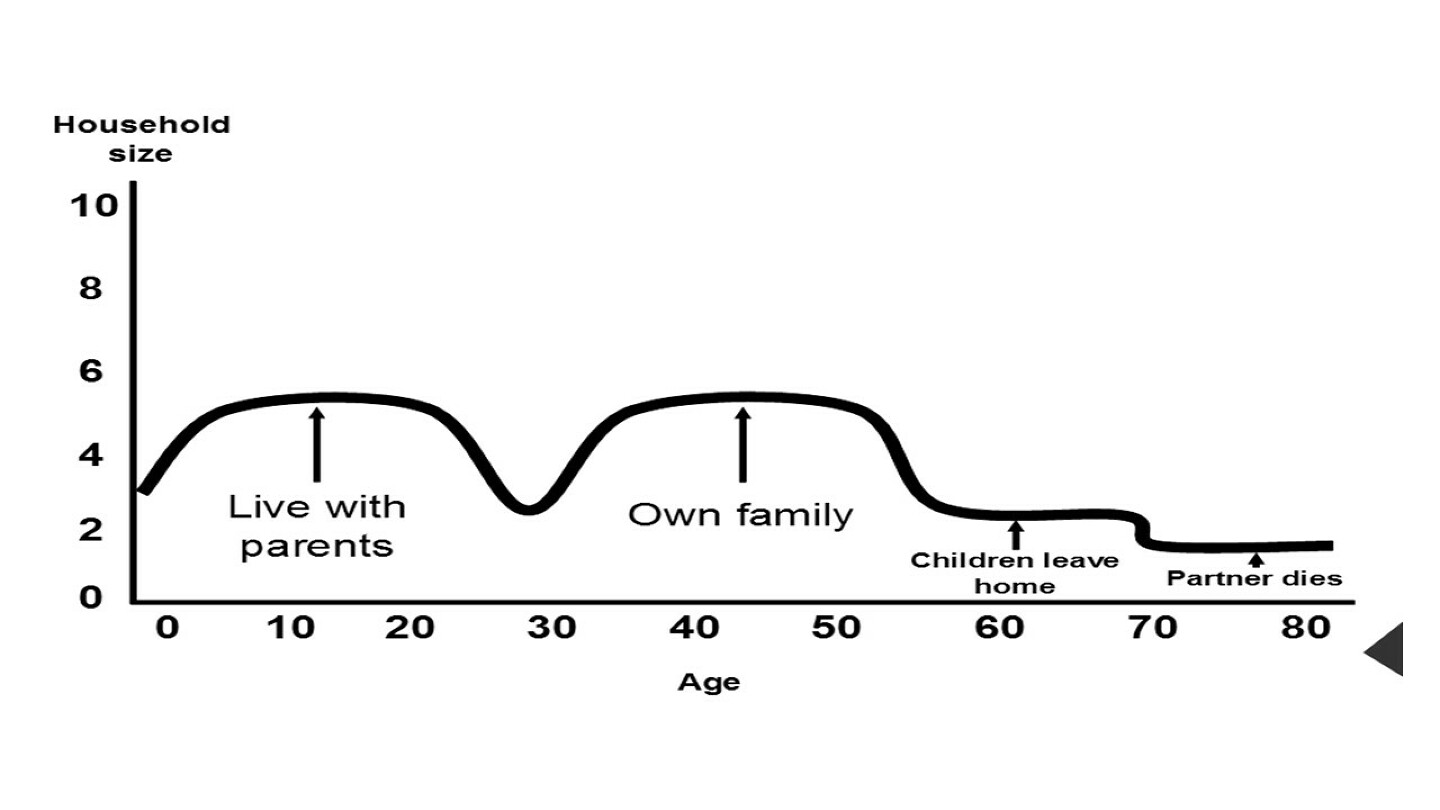

In the digital-first era of retail banking, aligning financial products and services with consumers' evolving needs is crucial for building trust, improving loyalty, and driving long-term profitability. Historically, life cycle stages were predictable, tied to age-related milestones such as education, employment, home ownership, and retirement.

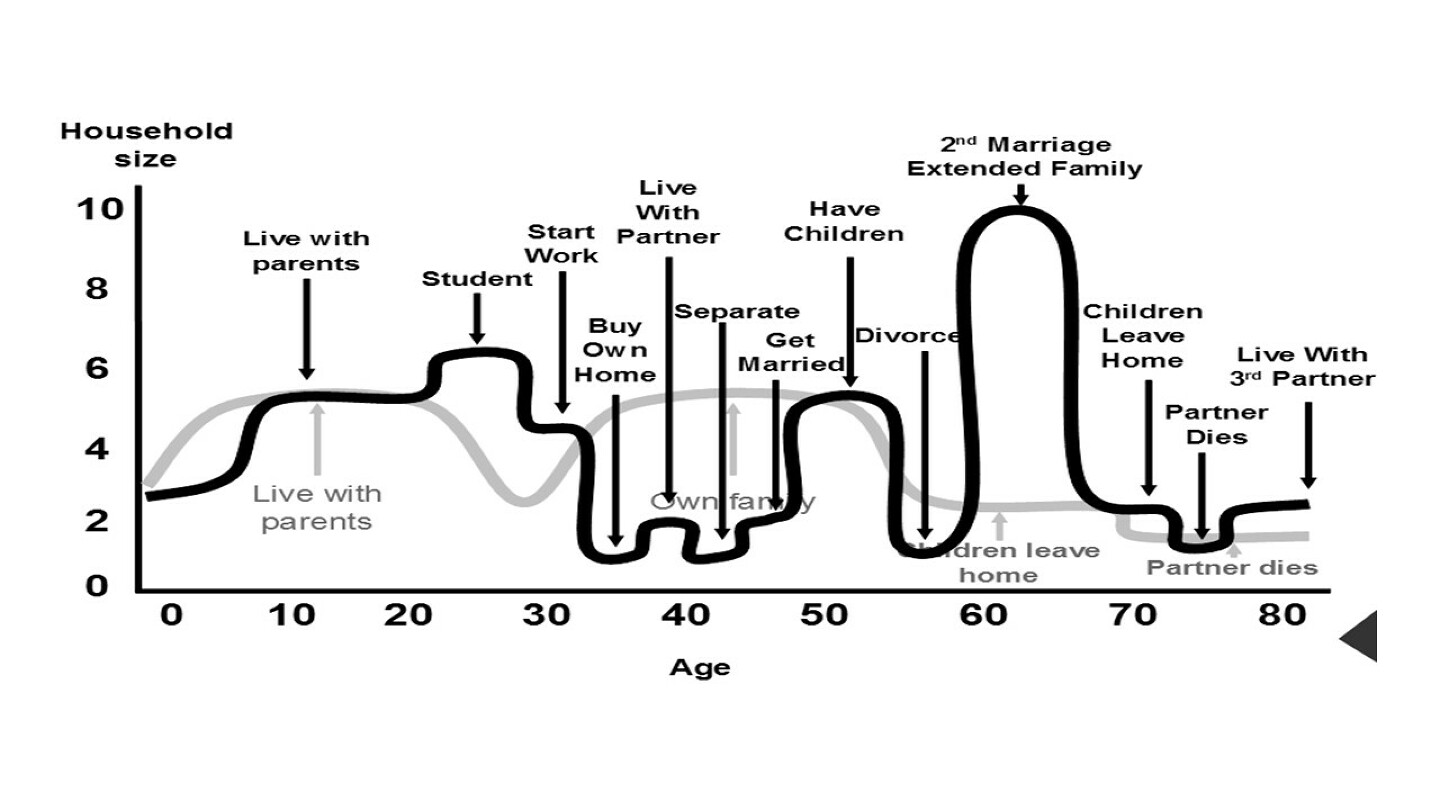

However, modern life stages have become more fluid, influenced by economic shifts, career changes, and longer life expectancy. (Traditional life stages are 'greyed out' and no longer align with modern, dynamic life stages.)

Traditional age-based segmentation is no longer sufficient. Instead, banks must leverage behavioural and transactional data to detect life events and provide relevant financial solutions in real time. AI-driven analytics, predictive models, and CRM systems allow banks to anticipate financial needs, ensuring proactive engagement rather than reactive service.

Data-driven Life Cycle Analysis

Banks use three primary data sources to understand consumer life stages:

- Internal Data: Transaction history, account activity, credit usage, digital interactions, and service engagement.

- External Data: Credit bureau reports, government statistics, real estate trends, and employment data.

- Customer Surveys: Direct feedback on financial aspirations, concerns, and preferences.

By integrating these sources, banks can map out key life transitions and offer personalised financial solutions at the right moment.

Life Stage Segments and Banking Needs

Young Adults (18-24): Typically students or early-career professionals, they require foundational banking services such as current accounts, digital banking access, and first-time credit products. Educational content on financial literacy and budgeting tools can grow engagement.

Young Professionals (25-35): With growing career stability, this segment seeks homeownership, savings plans, and insurance. Automated savings tools, mortgage comparison platforms, and AI-driven financial planning can support them.

Mid-Career (36-50): Focused on wealth accumulation, investments, and children's education, they benefit from advanced wealth management solutions, robo-advisors, and AI-driven financial insights.

Pre-Retirement (51-65): Prioritising long-term stability, this group needs retirement planning tools, estate management services, and hybrid digital-human financial advisory support.

Retirees (65+): Managing healthcare costs, retirement funds, and wealth transfer, they require simplified digital banking, fraud protection, and voice-assisted services for accessibility.

Beyond age groups, significant life events such as career changes, marriage, home purchases, childbirth, and retirement serve as financial inflection points. Banks that recognise and respond to these events with timely, relevant offerings can strengthen customer relationships and increase lifetime value.

MSME Life Stage Analysis vs. Consumer Life Stage Analysis

Similarities with Consumers

Both MSMEs and consumers experience life stages that dictate financial needs and behaviours. Consumers transition through personal milestones (education, homeownership, retirement), while MSMEs evolve from startup to growth, maturity, and exit. Banks can use their CRM systems and data analytics to track these transitions, ensuring personalised engagement and timely financial solutions. One important consideration is that MSME life stages are also closely linked to their owners' consumer life stages. By connecting both sets of data and insight, new deeper insights into the needs of MSME owners can be found and new opportunities realised.

Differences

- Life stage definition: Consumer stages are personal (education, career, family), while MSMEs follow a business trajectory (startup, growth, maturity, exit). We discuss these in the 'Understanding MSMEs to help them Succeed and Grow' module;

- Financial needs: Consumers seek personal financial products (loans, savings, retirement plans), while MSMEs require business financing, trade credit, and payroll management;

- Decision-making: Consumers decide based on personal and family goals, while MSME decisions involve multiple stakeholders, requiring tailored advisory services;

- Risk and revenue: Consumer banking risks stem from creditworthiness and income stability, while MSME banking presents higher revenue potential but greater market exposure and economic risks;

- Regulatory compliance: Consumer banking follows personal finance laws, whereas MSMEs face additional tax, trade, and business regulations;

- Engagement channels: Consumers use digital banking apps and branches, while MSMEs often rely on relationship managers and specialised business banking teams.

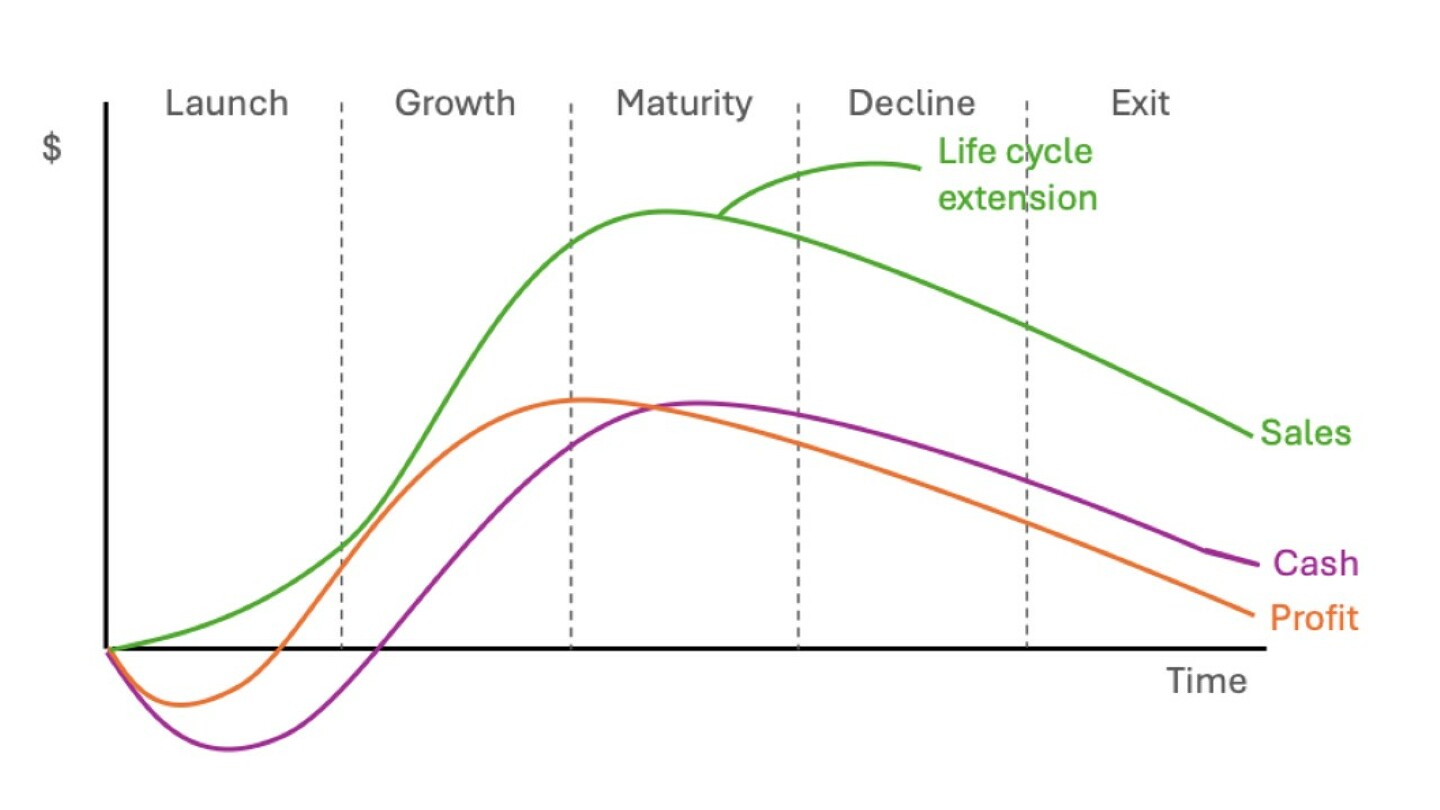

Five Stages of the Business Life Cycle

Like consumers, businesses have distinct stages that require targeted financial solutions:

- Start-up: New businesses with low sales and high costs face negative cash flow. Banking support includes startup loans, micro-loans, educational resources, and business banking accounts.

- Growth: Increasing sales, emerging profits, and positive cash flow. Banking support includes expansion loans, working capital financing, and cash management solutions.

- Maturity: Stabilised sales and profits, requiring efficiency and competitive strategies. Support may include expansion capital, risk management, and strategic partnerships.

- Renewal or decline: Businesses either innovate or face market saturation and decline. Banking Support may include restructuring loans, turnaround advisory, and innovation funding.

- Exit: Owners plan for business sale, merger, or closure. Support my include wealth management, tax advisory, and business transition planning.

In Summary

A customer-centric, data-driven approach to life stage analysis enables banks to deliver relevant and timely financial solutions. Whether serving individuals or MSMEs, leveraging AI, predictive analytics, and CRM insights ensures that banks remain proactive in meeting evolving financial needs. By aligning products and engagement strategies with life stages, banks can improve customer experiences, deepen loyalty, and drive sustainable growth in the competitive digital banking landscape.