Advanced Customer Management - Building Customer Management Capabilities

Customer Segmentation

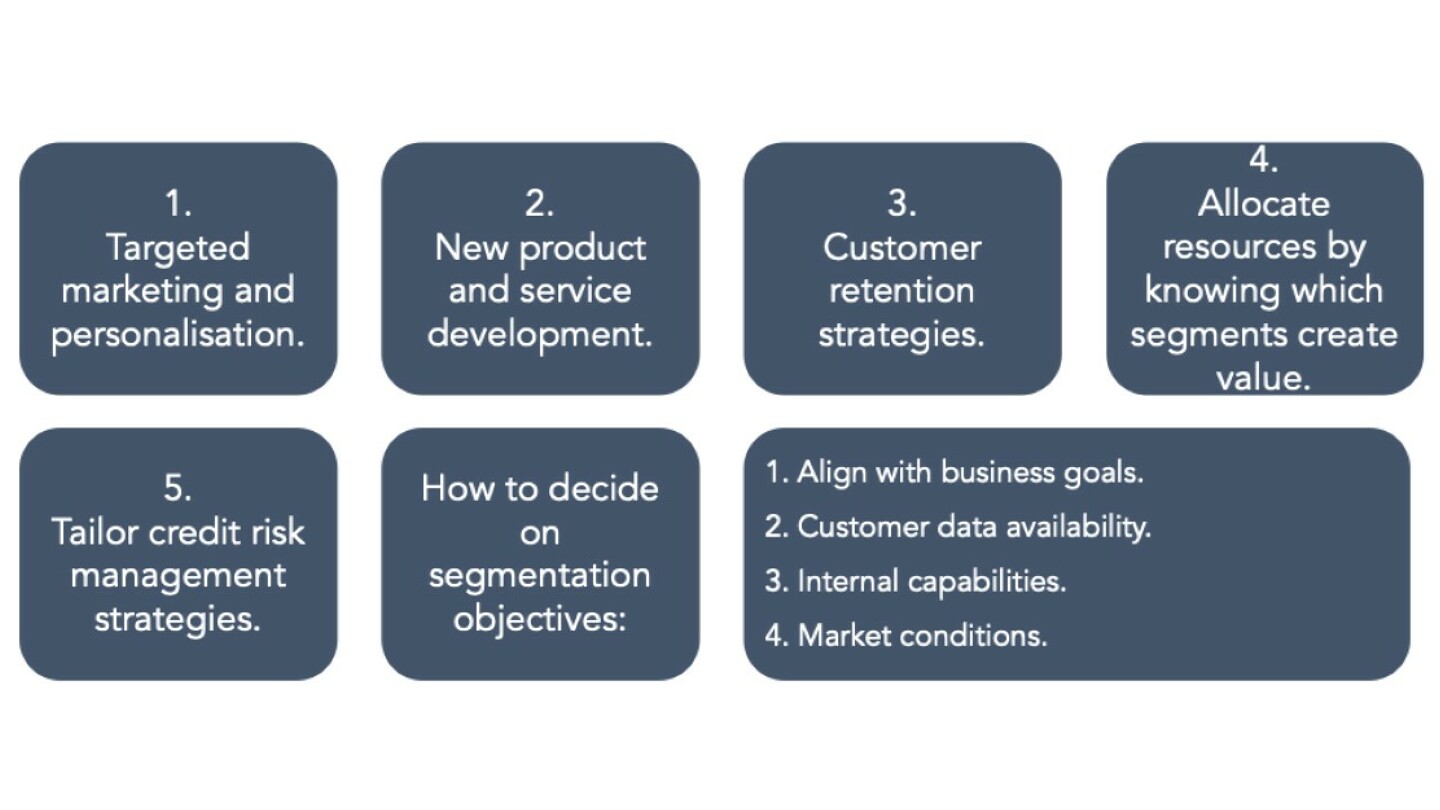

Customer Segmentation Underpins More than Marketing

Customer segmentation is a vital practice for retail banks, especially as they aim to offer increasingly personalised services to meet the unique needs of their diverse customer base. Behavioural segmentation focuses on grouping customers based on their behaviours, such as product usage, spending patterns, transaction history, and customer interaction. This approach empowers banks to provide tailored experiences, predict needs, improve marketing strategies, and grow customer loyalty.

Retail banks use segmentation to categorise customers and tailor products, services, and marketing strategies. The main types include demographic, geographic, behavioural, psychographic, life stage, and value-based segmentation. Each approach has its benefits and limitations, and banks often combine multiple methods for a more comprehensive strategy.

Main types of Segmentation

Retail banks and financial institutions use segmentation to categorise customers and tailor products, services, and marketing strategies effectively. The main types of segmentation include demographic, geographic, behavioural, psychographic, life stage, value-based, and MSME segmentation. Each approach has its advantages and limitations, and banks often combine multiple methods for a more comprehensive strategy.

Demographic Segmentation

Demographic segmentation groups customers based on age, income, education, occupation, and family status. It is widely used because it is easy to implement and helps target specific financial products, such as retirement plans for older customers or mortgages for young families. However, it can be too broad since people within the same demographic group may have different banking needs. Additionally, it does not account for behavioural differences or financial preferences, limiting its precision.

Geographic Segmentation

This categorises customers based on their location, such as country, city, or rural versus urban areas. This helps banks tailor services to local market conditions, regulations, and economic conditions. It is particularly useful for branch location decisions and marketing campaigns. However, with the increasing adoption of digital banking, geographic segmentation alone is becoming less relevant, as customers can access banking services remotely regardless of their physical location.

Behavioural Segmentation

Behavioural segmentation focuses on customers' interactions with the bank, including transaction history, product usage, spending habits, and digital engagement. It allows banks to predict customer needs, cross-sell relevant products, and personalise offerings. This segmentation is highly effective when combined with AI-driven CRM systems. However, it requires sophisticated data analysis and can raise privacy concerns if customers feel banks are tracking them too closely.

Psychographic Segmentation

This categorises customers based on their lifestyle, values, attitudes, and personality traits. This method provides deeper insights into customer motivations, allowing banks to align marketing strategies with customer aspirations. For example, risk-averse individuals may prefer conservative investment products, while risk-takers may seek higher-yield opportunities. However, psychographic data is very difficult to collect and measure, often requiring extensive surveys and qualitative research.

Life-stage and Value-based Segmentation

Life stage segmentation focuses on major life events such as starting a career, getting married, having children, or retiring. Banks use this to provide timely financial solutions, such as student loans for young professionals or retirement planning for older customers. This boosts customer relationships by addressing evolving financial needs. However, life stages are not always predictable, and banks must continuously update customer data to maintain accuracy.

Value-based segmentation prioritises customers based on profitability, assessing factors like total assets, product holdings, and revenue contribution to the bank. This helps banks allocate resources efficiently by focusing on high-value customers and offering personalised services. However, it may lead to the neglect of lower-value customers who could become profitable in the future. Ethical concerns also arise if banks disproportionately favour high-net-worth individuals.

MSME Segmentation

MSME segmentation focuses on micro, small, and medium-sized enterprises, a crucial customer group for banks, especially in emerging markets. MSMEs can be segmented by industry, business size, revenue, or financial needs. This approach helps banks provide tailored credit products, business advisory services, and digital banking solutions. However, MSME segmentation requires detailed financial data and risk assessment tools, as many small businesses lack formal financial records. Additionally, lending to MSMEs carries a higher risk, requiring banks to balance opportunity with risk management.

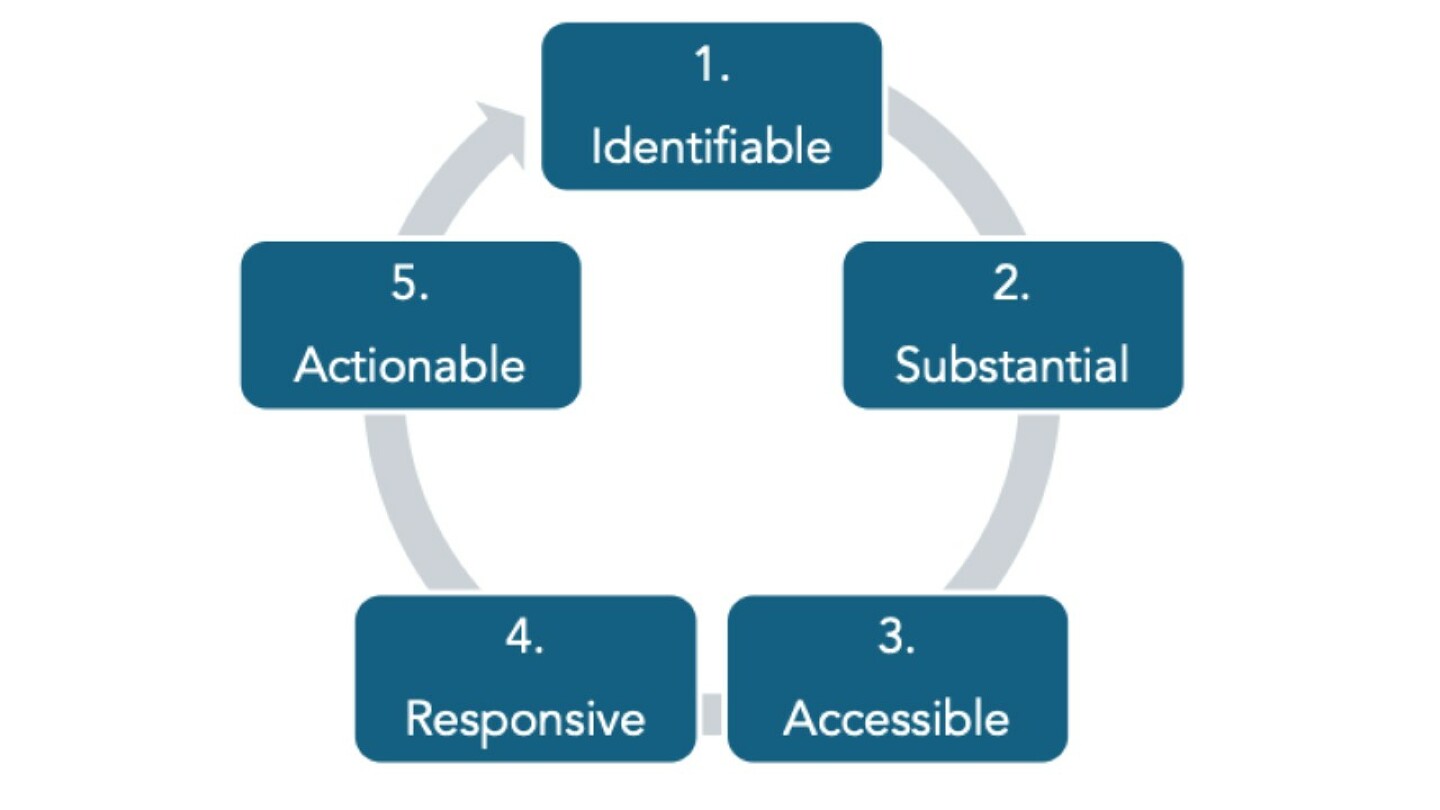

Segmentation must be:

- Able to find distinct groups in your portfolio. If it can't, then you cannot achieve the benefits described above;

- Profitable in terms of size or purchasing power;

- Reachable by marketing. Customers can select not to receive marketing material. If the segment has a high proportion of customers who have 'opted-out' from marketing approaches from the bank then it probably won't be worth pursuing. Bear in mind that employees often 'opt-out' customers from marketing without their permission to allow them to send marketing and stop direct marketing from marketing department. If they do this data protection regulation means that customers are 'opted-out' of all marketing! It can be useful to periodically ask customers to review their contact preferences, reenforcing how the bank will honour them;

- Proven responsive to marketing communications. If the segment doesn't respond to marketing then the bank will waste a lot of time and money;

- Reliable insight for marketing investment decisions. The process is circular, so banks need to continually improve their segmentation models. In fact, their first attempts may expose the need for more data or flaws in their reasoning.

Summary

No single segmentation method is sufficient on its own. The most effective strategies combine behavioural, life stage, value-based, and MSME segmentation, leveraging AI and CRM analytics for personalised engagement. As retail banking evolves, segmentation will remain a critical tool for delivering customer-centric financial services and fostering long-term customer relationships.

Benefits of Behavioural Segmentation

1. Personalised Marketing and Offers

Behavioural segmentation allows banks to deliver targeted marketing messages and offers to various customer segments based on their distinct behaviours. For example, customers who frequently use savings products may be offered investment opportunities, while those using credit cards may receive rewards, discounts, or limit increase offers.

2. Increased Cross-selling and Upselling

Behavioural segmentation helps banks identify customers more likely to benefit from additional products or services. For example, a customer who has used a personal loan product in the past may be offered refinancing options or new loan products aligned with their financial behaviours.

3. Improved Customer Retention

By understanding customer behaviour in detail, banks can proactively address issues before they lead to customer churn. If a customer exhibits signs of financial stress or is disengaging, a personalised outreach or financial planning service can prevent them from leaving.

4. Efficient Resource Allocation

Segmentation helps banks focus efforts on high-value customers or those showing the potential for higher value. Marketing and customer support resources can be deployed efficiently based on segment priorities, ensuring a higher return on investment.

5. Enhanced Customer Experience

Offering services tailored to each customer segment leads to better experiences, making customers feel understood, valued, and more likely to engage with the bank. These personalised interactions foster loyalty and satisfaction.

Challenges of Behavioural Segmentation

1. Data Complexity and Integration

A significant challenge is ensuring excellent integration of data from various touchpoints such as online banking, mobile apps, in-branch visits, and customer service interactions. Banks must have strong data management and analytics infrastructure to integrate and derive insights from disparate sources. For example, the behavioural data from a customer's in-branch visit must be combined with their online and mobile interactions to get a holistic view of their preferences and behaviour.

2. Privacy Concerns and Regulatory Compliance

Banks are required to comply with a myriad of data protection regulations like GDPR, CCPA (California Consumer Privacy Act), and other local privacy laws that impose strict guidelines on how customer data is collected, processed, and stored. While behavioural segmentation relies heavily on customer data, it's essential that banks implement ethical and secure data usage practices to ensure they are not infringing on customers' rights or breaching any legal requirements.

AI Challenges

The use of AI in behavioural segmentation raises important ethical considerations. AI models used for data analysis and segmentation rely heavily on large datasets, often synthesising new data points based on observed patterns. While this can improve predictive analytics and segmentation, it also presents privacy risks if the data is not anonymised, or if algorithms inadvertently perpetuate biases.

Banks need to ensure that AI tools used for segmentation adhere to ethical guidelines, maintaining transparency and accountability for how data is used, ensuring customers' rights are respected. Additionally, AI algorithms must be regularly audited for fairness and accuracy to prevent discriminatory practices or unintended consequences.

3. Over-reliance on Past Behaviour

While past behaviour is a strong indicator of a customer's preferences, it can lead to challenges, particularly when predicting future behaviour or addressing rapidly changing needs. Relying solely on past behaviours might cause banks to overlook emerging trends or shifts in customer preferences, leading to missed opportunities or suboptimal service offerings.

Predictive Analytics

Predictive analytics uses historical data to forecast future outcomes and customer behaviour. While it can be a valuable tool in behavioural segmentation, it's important not to solely rely on past behaviours. For instance, a customer who traditionally deposits a set amount every month but suddenly reduces this amount could indicate financial stress or a new spending habit that isn't immediately apparent from previous data.

Predictive analytics can help mitigate this by identifying early warning signs and adapting segmentation models dynamically to reflect changing behaviours, ensuring that the bank's actions remain aligned with the customer's evolving needs.

4. Dynamic and Evolving Customer Behaviours

Customer behaviours are constantly evolving, making it difficult to maintain relevant segmentation. For example, a customer might shift from being a casual user of digital banking to becoming a heavy user during a financial crisis, requiring the bank to adjust segmentation regularly. Additionally, customers may display seasonal or situational changes in behaviour, such as increased spending around holidays or during significant life events (e.g., buying a home, getting married). Segmentation needs to be agile enough to respond to these changes.

5. Technological Investment and Skills

Developing and maintaining the technological infrastructure to analyse and act on behavioural data requires significant investment and skilled personnel, which can be a barrier for smaller banks. Ensuring banks have the technology to collect, store, and analyse large volumes of behavioural data is a continual challenge, especially as data privacy regulations tighten.

How Personas Are Created and Used in Behavioural Segmentation

Personas are detailed, data-driven representations of customer segments, designed to humanise the data and make it more actionable. They are crucial in personalising marketing, communication, and product offerings. Here's a more detailed look at how personas are created and how they are used:

1. Data Collection and Analysis

Banks collect data across multiple channels like mobile apps, websites, branch visits, and customer service interactions. By analysing behaviours such as frequency of transactions, product usage patterns, transaction history, and lifestyle factors, they can group customers into specific personas based on shared characteristics.

2. Identifying Key Behavioural Characteristics

Once data is collected, banks identify common behaviours within each segment. These characteristics might include spending habits, lifestyle preferences, financial goals, or engagement frequency with specific products or services.

3. Persona Development

Based on the data analysis, banks create personas that represent the typical customer within a behavioural segment. A persona may include details contained in these three examples:

Name: The Savvy Saver

Age: 26

Behaviour: Regularly deposits funds into a savings account, uses a rewards-based credit card for everyday purchases, frequently checks balances on mobile app.

Financial Goals: Save for a down payment on a home.

Pain Points: Difficulty finding investment options that align with her conservative risk appetite.

Preferred Channels: Mobile app, digital support, email.

Mobile App Usage: Actively uses budgeting tools and savings features, and tracks progress on goals.

Another persona might be:

Name: The Young Professional

Age: 32

Behaviour: Active on mobile and online banking channels, uses a rewards-based credit card, often makes international transactions due to frequent overseas travel, checks balances daily, has a growing interest in building credit.

Financial Goals: Build a strong credit profile, save for a future home, manage travel expenses.

Pain Points: Difficulty tracking overseas spending and managing credit card fees associated with international use.

Preferred Channels: Mobile app, email, in-app notifications.

Mobile App Usage: Frequently uses budgeting and money management tools, tracks spending and sets up alerts for international transactions.

Prospective Customer Persona:

Name: The Prospective Switcher

Age: 40

Behaviour: Considering switching bank accounts due to dissatisfaction with current provider's digital experience. Is exploring a bank with a robust mobile app that offers budgeting and money management tools.

Financial Goals: Streamline financial management, simplify budgeting and spending, find a bank that aligns with digital-first preferences.

Pain Points: Poor mobile app experience with current bank, cumbersome budgeting tools, lack of personalised financial insights.

Preferred Channels: Primarily mobile app and website, with occasional in-branch visits to resolve more complex issues.

Mobile App Usage: Looking for a bank with strong budgeting tools and personalised financial insights, comparing different bank features to find the best fit.

4. Validation and Refinement

Personas should be regularly reviewed and updated based on new data and customer feedback to ensure they remain accurate and relevant. Banks can adjust personas based on evolving trends or changes in customer preferences.

Using Personas in Behavioural Segmentation:

1. Targeted Marketing Campaigns

Personas help banks design highly relevant marketing messages and offers tailored to each segment's behaviour. For example, The Savvy Saver could receive a targeted campaign promoting a high-yield savings account or investment advisory services, while The Young Professional might receive offers for internationally-focused credit cards or travel-related financial services.

2. Personalisation

Banks can use personas to deliver personalised experiences, ensuring that customers feel the bank is addressing their unique needs. The Savvy Saver might be offered tools for automated savings and budgeting tools that help her reach her savings goals, while The Young Professional might receive travel rewards based on his frequent international purchases, along with a no-foreign transaction fee credit card offer.

3. Turning Prospects into Customers

Personas can also help convert prospects into customers by highlighting features that appeal directly to them. For example, The Prospective Switcher could be targeted with an easy account switch programme combined with highlighted features like an intuitive mobile app, personalised budgeting tools, and streamlined digital account management.

4. Customer Service Optimisation

Personas guide customer service teams to handle interactions more effectively. For example, if a customer identified as The Savvy Saver calls the bank, the representative will know that she prefers digital solutions and may provide information related to digital banking tools, auto-savings programmes, or investment opportunities tailored to their goals.

Summary

Behavioural segmentation allows banks to offer personalised, customer-focused services, but it is crucial to manage the challenges carefully. Banks must ensure ethical data usage, adapt to changing behaviours, and avoid over-reliance on past data to stay ahead of customer needs.