Fintech Revolution

From Disruption to Partnership

Traditional banks worldwide initially dismissed fintechs and neobanks, believing digital-only financial services wouldn't gain customer trust. Banks relied on strict regulations and customer apathy as hurdles to protect them, assuming challengers like PayPal, Square (now Block), and LendingClub in the U.S., Alipay and WeChat Pay in China, and mobile money players in Africa would struggle with compliance. As a result, most banks made only minor digital improvements, confident fintechs would fail or, at worst, remain niche players.

By 2015, fintechs started to gain traction globally. In Europe, Revolut, Monzo, and N26 started to disrupt traditional banking. In Asia, Ant Group, Grab Financial (Malaysia), and Paytm (India) redefined payments and lending. In Latin America, Nubank (Brasil) and Mercado Pago (Argentina) offered digital banking, while in Africa, startups like Flutterwave (Nigeria), Chipper Cash (Nigeria), and TymeBank (South Africa) provided financial access to the previously unbanked. Banks responded by acquiring fintechs, forming partnerships, and finally launching digital-first platforms.

Today, traditional banks increasingly collaborate with fintechs to enhance efficiency and reach underserved markets. Open banking in Europe, QR-code-based payments in Asia, digital mobile wallets in Africa, and crypto-driven finance in Latin America show how fintechs are reshaping global banking.

Initially, fintech founders saw banks as outdated and bureaucratic, but many underestimated the need for trust, compliance, and long-term stable capital. Over time, firms like Chime, SoFi, and Robinhood in the U.S. and Ualá (Argentina), and Judo Bank (Australia) shifted from pure disruption to ordered growth.

Now, fintechs recognise banks' resilience, while banks embrace fintech innovation: the battle has evolved into collaboration.

In this module we'll define and discuss the emerging financial landscape that includes traditional retail banks, fintechs, neobanks and new non-financial services players such as telcos and tech giants who are adding financial services to their core business of telecommunications, ecommerce, consumer electronics, social media or digital advertising.

Why are telcos and tech giants now offering financial services? To convert their trust, scale, and data into recurring, high-margin revenues while reinforcing their ecosystems.

Is the Fintech Revolution Over or Just Beginning?

The fintech revolution is far from over: in fact, it's entering a new phase. While the first wave of fintechs, neobanks, and digital disruptors have reshaped financial services, the industry is now moving toward deeper integration, regulatory compliance, and competition from new players like big tech, and decentralised finance (DeFi). The question is no longer whether fintechs will survive, but which ones will scale sustainably.

Scaling to Commercial Sustainability

Starting a new fintech or neobank digital-only bank is risky. Key survival factors include regulatory compliance, an on-going capital access, a tight product-market fit, strong customer experience, and sustainable lifetime value exceeding customer acquisition costs. If these factors are achieved, profitability is usually achieved after six or seven years of operations (venture capitalist investors usually look for an exit plan by this point). Key failure factors include unclear and narrow propositions causing customer misalignment, poor engagement and monetisation challenges, weak market differentiation in a saturated market, unsustainable funding 'burn rate', regulatory tightening that makes the business model unsustainable, and investor misalignment causing finding to dry-up. Ten-year failure rates can be as high as 90% depending on the business model chosen.

Very often a start-up fintech or neobank won't shut down all accounts (perhaps except in the case where the regulator forces them) and close. Instead the owners will look to salvage as much as they can from investments made by selling the customer base and/or technology, merging with another business, or pivoting to a different business model. Wise (formerly TransferWise) successfully pivoted from person-to-person low-cost remittances to multicurrency accounts and debit cards to broaden their revenue model.

Digital-first Banks are Dominating Customer Satisfaction

By 2030, fintechs and neobanks will no longer be seen as radical disruptors but as established financial players. Many early fintechs have expanded into full-service digital banking. Others will consolidate, partner with traditional banks, or be acquired.

Customer satisfaction surveys reveal traditional banks are losing ground to digital-first rivals, which offer faster, more convenient, and personalised service. Satisfaction reflects trust, loyalty, and retention – key drivers of engagement and revenue. As expectations rise, traditional banks struggle with slow digital transformation, outdated systems, reduced services, and branch closures. Once known for reliability, they're no longer the preferred choice for informed consumers, who now favour tech-driven alternatives that better meet their evolving needs.

Digital-first retail banks have topped the UK's official bank customer satisfaction survey (conducted by Ipsos on behalf of the Competition and Markets Authority that is displayed on all bank websites and in all branches) for the last five years in a row.

These digital-first banks are relative newcomers: Monzo (launched in 2015), Starling Bank (2016), Chase UK (2021), Metro Bank (2010), and First Direct (digital-first bank, part of HSBC UK) in 1989. By comparison Nationwide (a mutual owned by its members, not shareholders) launched in 1884, and Lloyds Bank in 1794 (ranked sixth place). Other large UK banks, such as Barclays (10), NatWest (11), HSBC (12), and Santander (12) haven't featured in the top five since Monzo and Starling Bank were added to the survey of 17 banks in late 2020. As the UK was an early mover on issuing digital banking licences, this may carry lessons for other countries.

Net customer growth figures show a corresponding trend, with the top five in 2025 acquiring more customers than they lost, and the bottom 12 generally losing more than they acquired. This happened despite offering generous monetary incentives to customers who switched their current account from a competitor.

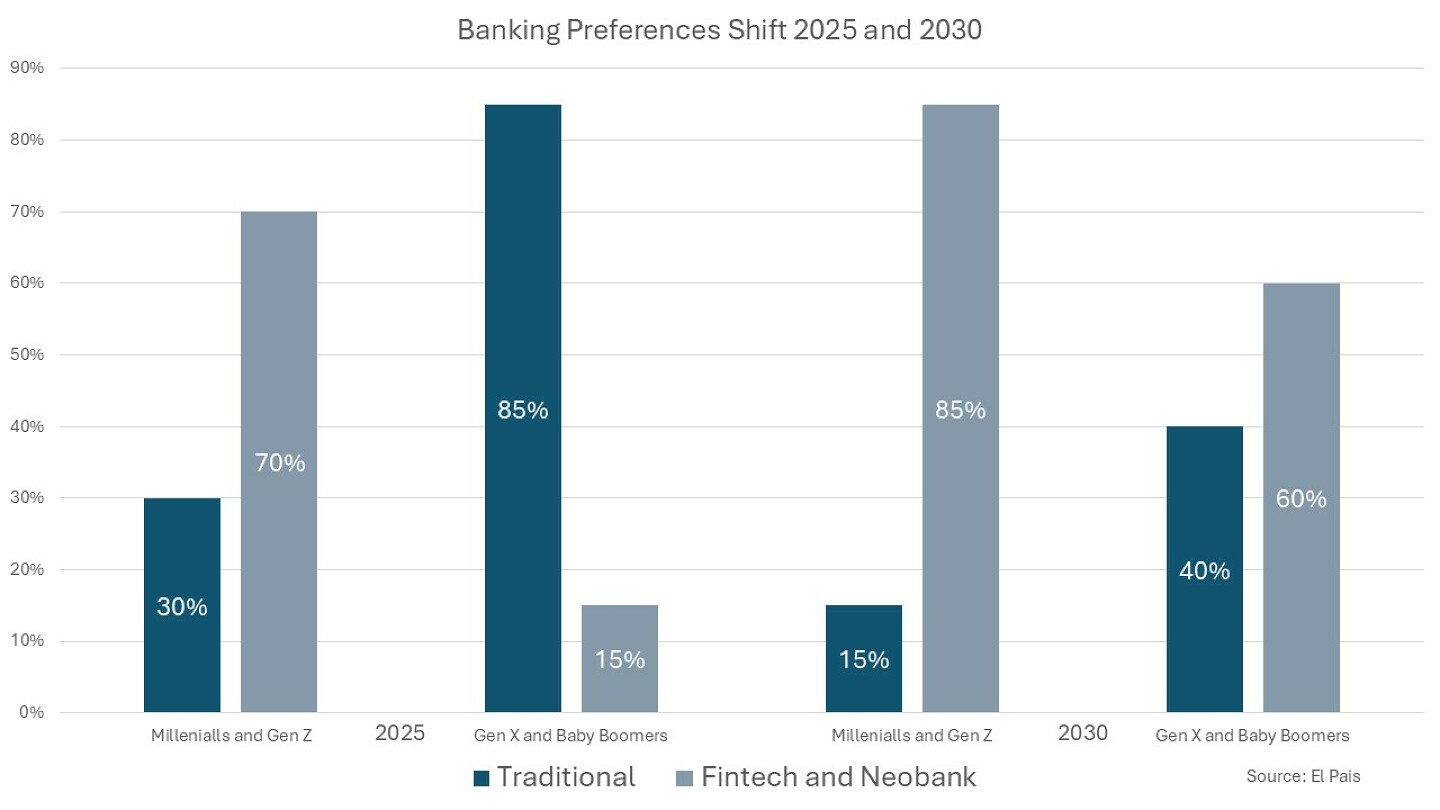

While precise generational data is scarce, anecdotally, the digital nature of Monzo, Starling Bank, and Chase UK suggests they attract a diverse customer base, with a notable emphasis on younger consumers. As the following graph shows, the shift from traditional banks to fintechs and neobanks will become even more pronounced by 2030.

There could not be a clearer warning signal for traditional retail banks!

Traditional Banks Are Adapting

Banks that once dismissed fintechs have embraced digital transformation. By 2030, we expect to see most major banks operating fintech-like digital subsidiaries or integrating AI, blockchain, and embedded finance into their operations and offers. However, the challenge for banks will be balancing legacy infrastructure, regulatory burdens, and evolving customer expectations.

An example of bank adaptation is the growth of national payment wallets in Europe, which let customers transfer money using a mobile number. Banks have collaborated at national level to build interoperable payment systems such as Blik (Poland), Swish in Sweden, Twint in Switzerland and MB Way in Portugal.

Big Tech's Growing Role

Companies like Apple, Google, Amason, Tencent (China) and others are expanding their financial services, leveraging their platforms for payments, lending, insurance, and wealth management. The real disruption has come from 'super apps' (like WeChat Pay, owned by Tencent, and Grab), which integrate banking effortlessly into daily life, making traditional banking increasingly invisible.

AI, Blockchain, and Decentralised Finance (DeFi)

By 2030, AI-driven banking, real-time credit decisions, and blockchain-based payments may be standard. DeFi could challenge traditional finance further, but widespread adoption depends on regulatory frameworks and consumer trust. US regulators in particular are becoming more supportive of cryptocurrencies while globally, central banks are experimenting with central bank digital currencies.

Regional Differences and Financial Inclusion

In Africa, Latin America, and Southeast Asia, non-traditional players will continue to drive financial inclusion. Mobile money platforms such as M-Pesa, Airtel, and MTN's MoMo, Flutterwave (Nigeria), and Ualá (Argentina) will expand their offerings, while traditional banks will either collaborate or risk losing relevance.

The Next Decade of Revolution

The fintech revolution isn't over: it's evolving. By 2030, financial services will be a blend of fintech innovation, digital-first banking, and big tech finance, with AI and blockchain reshaping the landscape. The winners will be those who can integrate these advancements while maintaining trust, compliance, and customer-centricity.