Corporate Governance In Banking

Scenarios of Corporate Governance in the Future

With respect to how corporate governance can deal with the predominance of intangible assets over tangible ones, the response is two-fold. On the one hand the organisation needs to develop a strong corporate culture that commits to protecting and enhancing intellectual capital in all its forms: human, structural and relational. For this to happen the Board of Directors must operate through the 'Board of Directors vs CEO' governance relationship to ensure that senior management is acting through the 'CEO vs rank & file' governance relationship to construct that corporate culture. On the other hand, the organisation must strive to be able to account for and thus manage intellectual capital. The Integrated Report is a promising initiative to do exactly that. (The Integrated Report is a concise communication about how an organisation's strategy, governance, performance and prospects, in the context of its external environment, lead to the creation of value in the short, medium and long term. It was created by the International Integrated Reporting Council (IIRC), a worldwide coalition of regulators, investors, companies, standard setters, the accounting profession and NGOs.)

With respect to how to adapt corporate governance to deal with multiple stakeholder groups many of which may have opposing interests, is a key aspect that needs to be looked at carefully by the Board of Directors. Of course, the world was easier in the industrial era when "the business of business was business" and there was only one overarching stakeholder group (the shareholders), but the need for sustainability has led to this new reality where the organisation must deal with multiple stakeholders.

In this space the organisation needs to make tough decisions; it is about prioritising amongst competing sustainability initiatives and thus stakeholders. As long as the organisation is clear in its priorities and transparent with its stakeholders, it will be able to defend its position effectively. The Board of Directors needs to ensure that management is informing the stakeholders and that the Board itself interacts proactively with them. We arrive at the key conclusion that Boards need to move beyond the agency problem as filling the information gap between management and the stakeholder groups is a lost battle. It is far more productive to develop a corporate culture of 'performance with integrity' as the best protection for the interest of stakeholders.

In terms of the challenges of digitalisation and the cybersecurity risks that come with it, requires having in place appropriate governance and compliance controls that will reinforce a corporate culture oriented to protecting and enhancing the organisation's intellectual capital. This, in turn, generates a positive spiral of improving governance/compliance controls processes, systems and competencies. Achieving this positive spiral requires making good decisions in terms of technology. It also requires ensuring an optimal human-machine interaction taken to new levels, promoting knowledge sharing between people, and applying technology to carry out multi-dimensional bio-recognition.

Finally, it should be clear the pivotal role the governance relationships of 'Board of Directors vs CEO' and 'CEO vs rank & file' play in achieving an effective corporate governance in the knowledge economy.

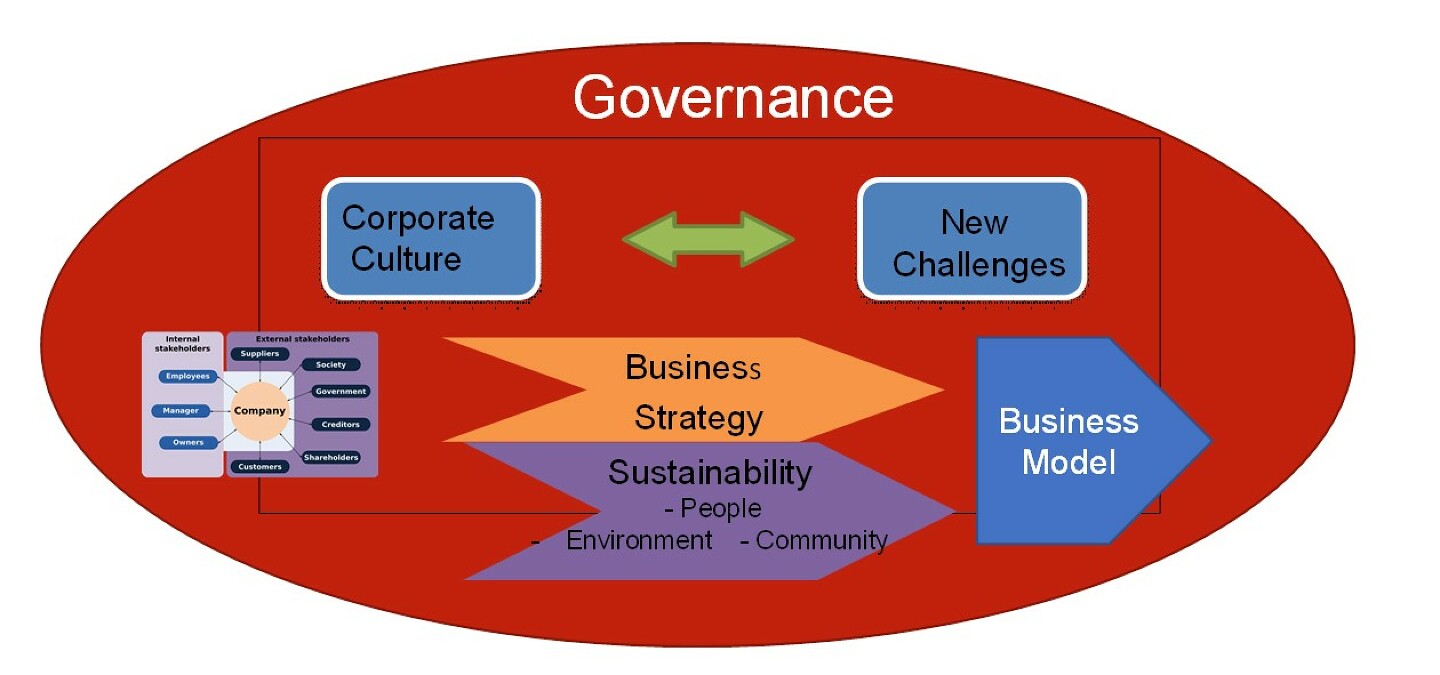

So, what changes need to be incorporated into corporate governance to cope with the challenges posed by the transition to a knowledge economy? The short answer to this is that in the knowledge economy Boards of Directors need to go beyond the agency problem that was their traditional concern. The Board must now focus on monitoring that the organisation develops a robust corporate culture that promotes 'performance with integrity' and that enhances its key intangible asset, intellectual capital. Most important of all, corporate governance itself moves from being just one dimension of sustainability to becoming the great integrator that ties together corporate culture, stakeholder management, and a sustainable business strategy that addresses the organisation's new challenges in an innovative business model, as represented in figure 2.

Topic for Reflection: Read chapters 7 and 8 of the book and carry out the following: Research the Wirecard accounting fraud case and apply all the corporate governance concepts of the course to explain the phenomenon. What can be done to avoid a case like this happening again in the future?